Will the stock market party continue in 2025?

Redacción Mapfre

Monthly report from MAPFRE Gestión Patrimonial

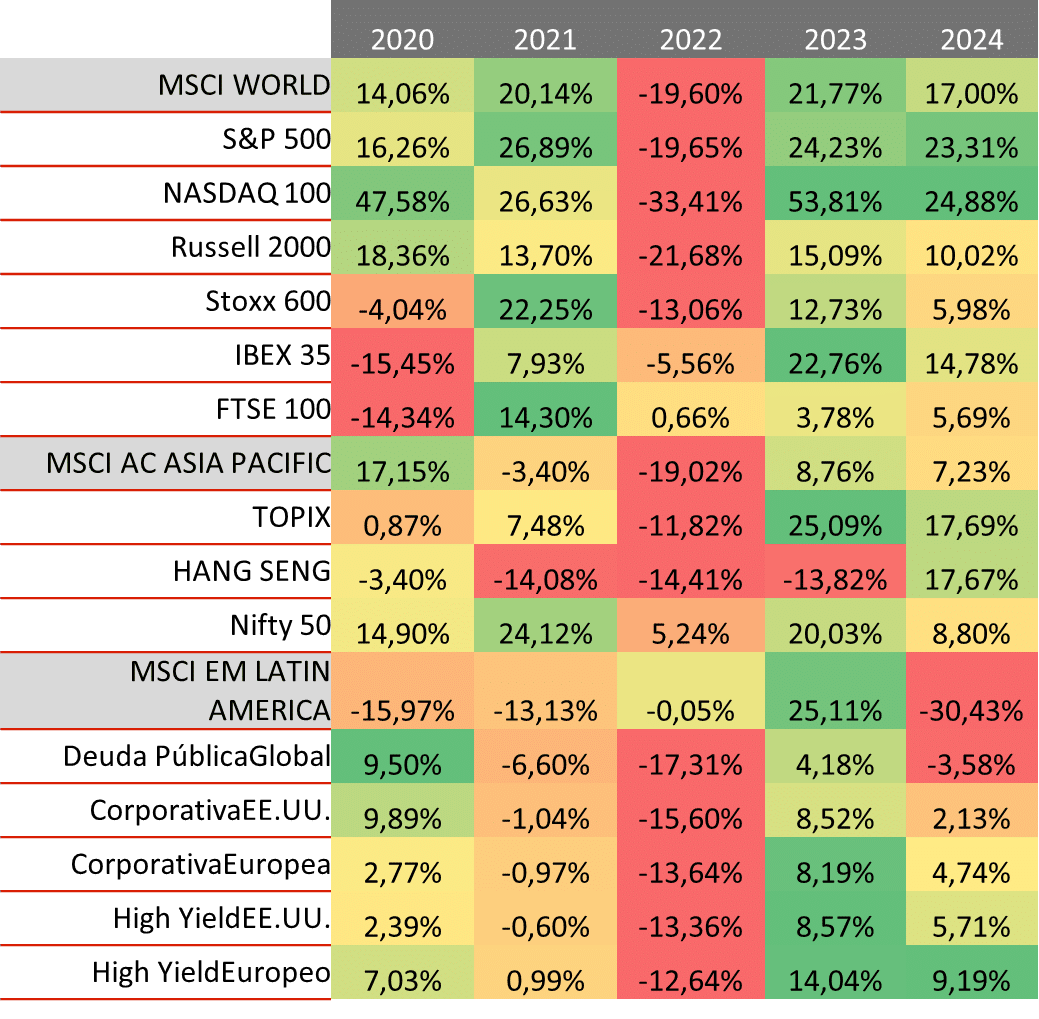

The stock market defies traditional economic principles more often than one might expect, with investor sentiment playing a significant role in shaping the future valuation of financial assets. 2024 ended without the typical December Santa Claus rally, but it still left behind a year marked by steady performance across major assets and more than respectable returns for the full 12-month period (figure 1).

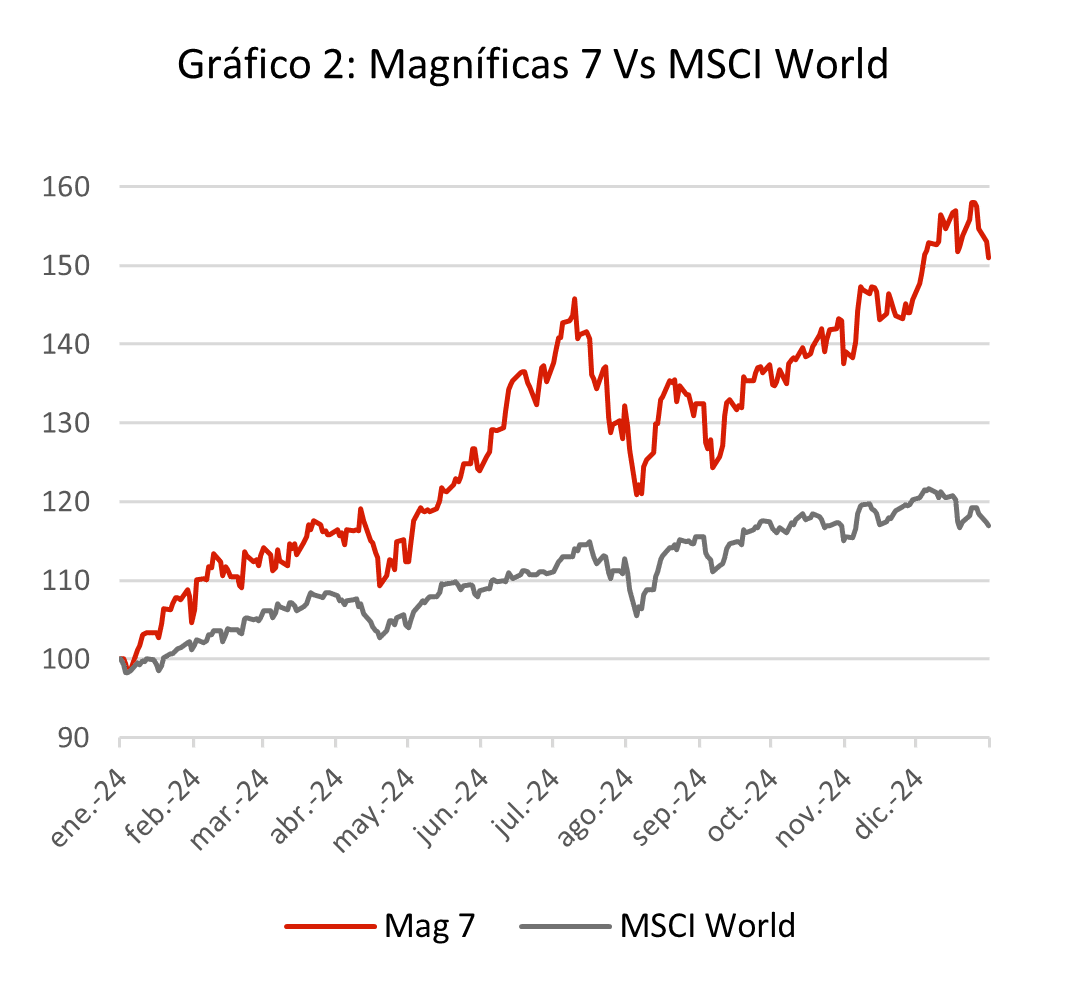

The strong performance of economies, which weathered the sharp rise in interest rates over the past two years and saw a significant reduction in inflation, provided key support for investors when evaluating different assets. It was also a year marked by a divergence in performance between the United States and Europe. On the equity side, U.S. indices returned more than 20% for the second year in a row, while European indices posted more modest gains.

Looking at fixed income, relative performance of European bonds weakened as the European Central Bank (ECB) adopted a more active stance and provided a clearer monetary policy path compared to the Federal Reserve (Fed). It was also a year in which large-cap companies outperformed their small-cap counterparts, with the Seven Magnificent (Apple, Nvidia, Amazon, Microsoft, Tesla, Google, and Meta) surging by 50% (figure 2).

The key question now is whether the 2024 market party will continue into 2025, or if the inevitable hangover will set in. In this regard, January and February typically set the tone for the rest of the year. This sentiment will be heavily influenced by the political landscape in early 2025, as it coincides with Donald Trump's return to power, elections in Germany, and political instability in France. As such, we'll likely have to wait until mid-Q1 to get a clearer picture of what to expect in 2025, although the consensus is currently for another year of market optimism.

Will the final 2024 scenario hold up in 2025?

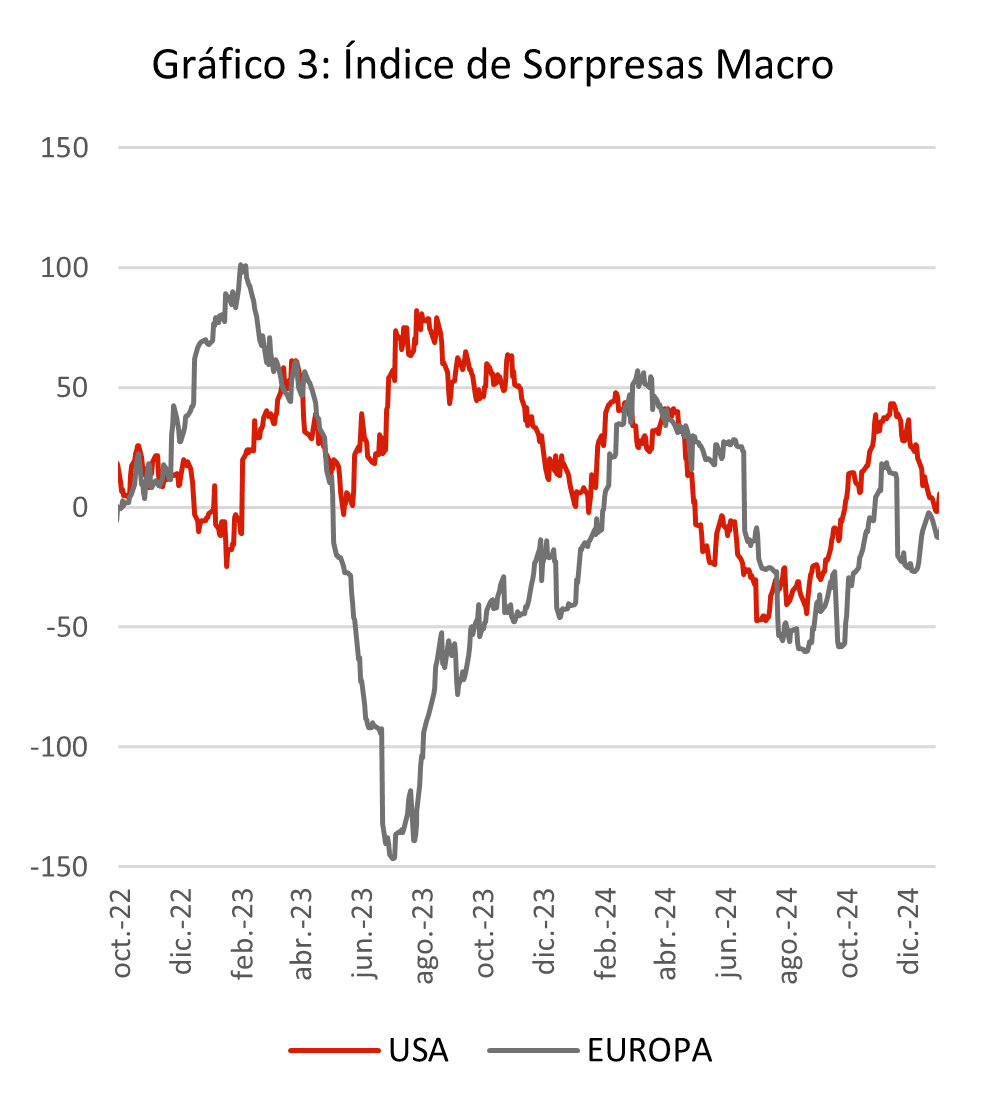

From a growth perspective, the answer to this question is clearly yes. Sentiment towards the Eurozone, and France and Germany in particular, remains extremely negative. So much so that it seems hard for conditions to deteriorate further, suggesting that the worst-case scenario may already be priced in, and any unexpected developments could be upside surprises. In fact, in the final weeks of the year, we began to see signs of improvement, as reflected in the macroeconomic surprise index (figure 3) for the Eurozone.

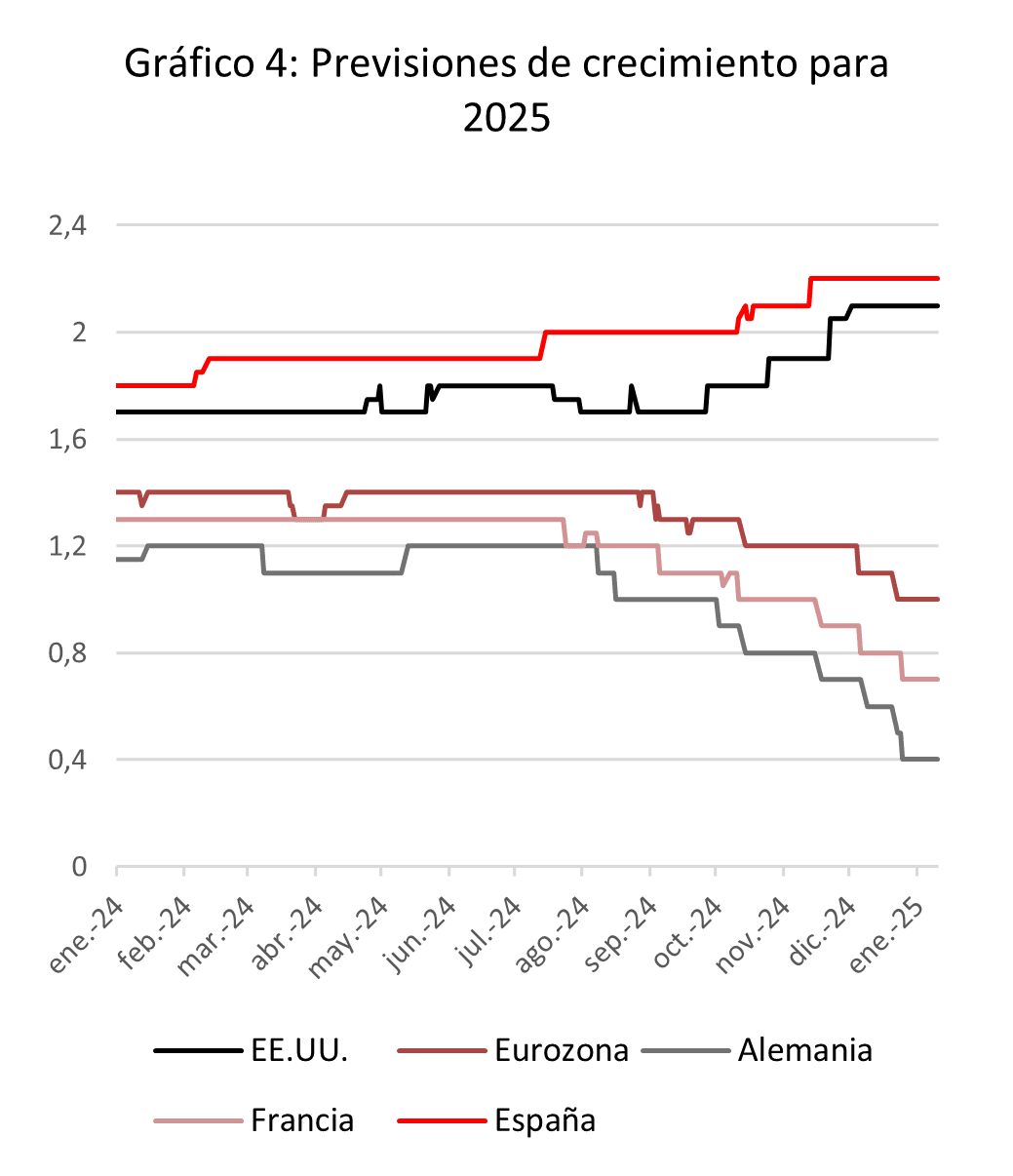

The economic principles we mentioned earlier in this report would suggest that growth in Europe should be improving, but so far the data hardly support this view. Looking at the United States, growth forecasts for 2025 are clearly positive. All the measures announced by Trump are pro-growth, and for those that may not be as growth-friendly (such as tariffs), there is no clear consensus on their potential impact. As a result, the growth forecast has been revised upwards by almost half a percentage point following the outcome of the US election (figure 4).

But these first two months of the year will also serve to test the ability of the new US president to implement the measures announced or discussed during the election campaign. Even more importantly, it will be crucial to observe the political reactions of the countries most affected, such as China, Mexico, Canada, and the Eurozone. It’s possible (though unlikely) that these countries could introduce policies aimed at countering Trump's actions, and if successful, this could be enough to restore market confidence, which is currently firmly and almost exclusively on the North American side.

The challenge of inflation in 2025

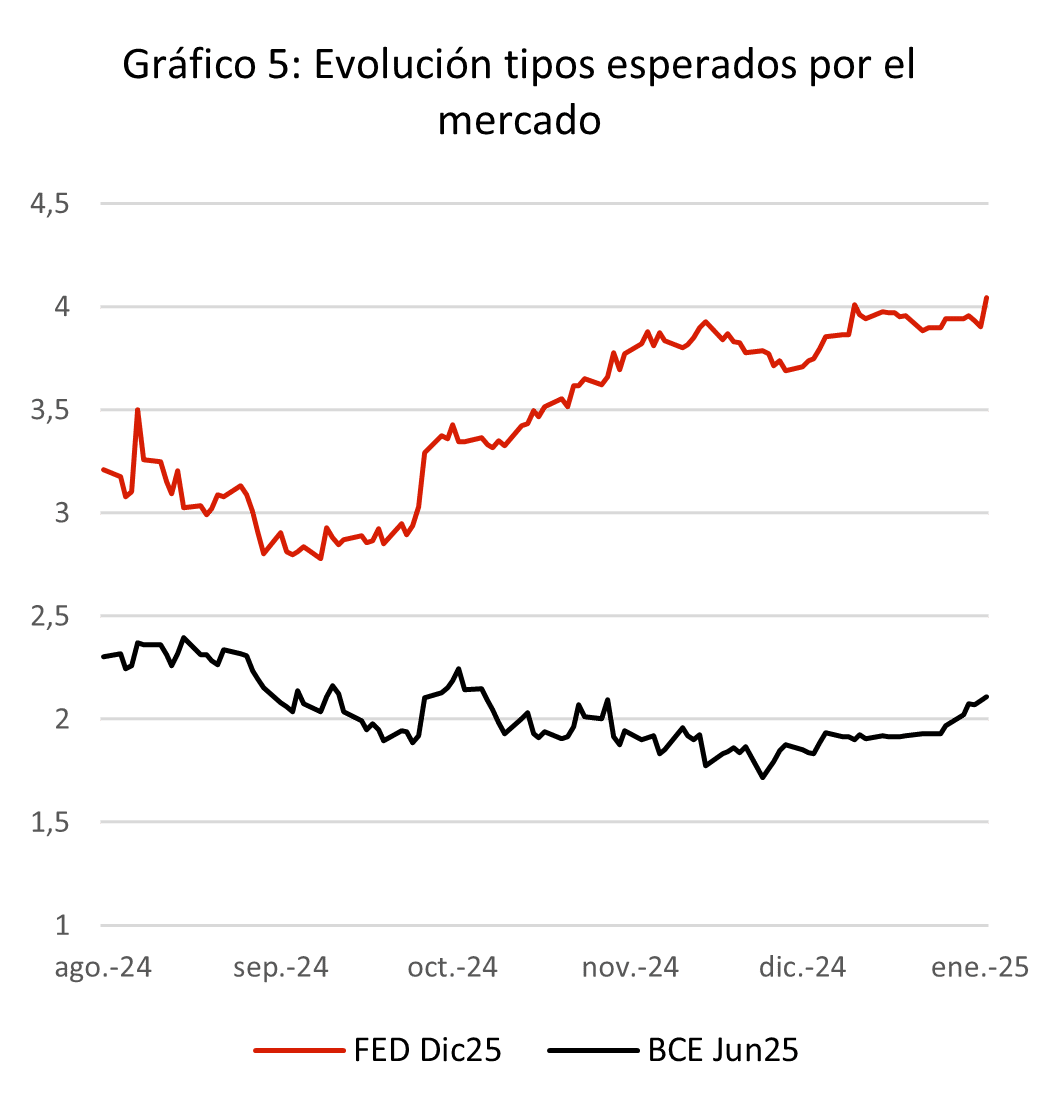

While long-term inflation expectations have remained stable, inflation is once again emerging as a key risk that many economists are highlighting for 2025. Some of the measures mentioned in our previous report that Trump could implement are likely to result in higher inflation, and the market has already started to reflect this, with an uptick in the levels at which it expects central banks to halt interest rate cuts (figure 5).

After all, growth of 2% in the United States and 1% in Europe, coupled with inflation rates of 2.5% and 2%, respectively, would leave little room for further cuts in official interest rates from current levels. If it’s confirmed that Trump will follow through on his immigration and tariff policies, and if growth in Europe surprises to the upside due to increased fiscal spending and/or a rebound in demand from China, central banks will likely need to adjust the trajectory of rate cuts they had completed in 2024. These cuts haven’t resulted in lower funding costs for governments and corporations, as long-term interest rates have risen despite the 100 basis point cuts by the Fed and the ECB, with required yields ending the year higher than where they began.

Liquidity reaches the real economy

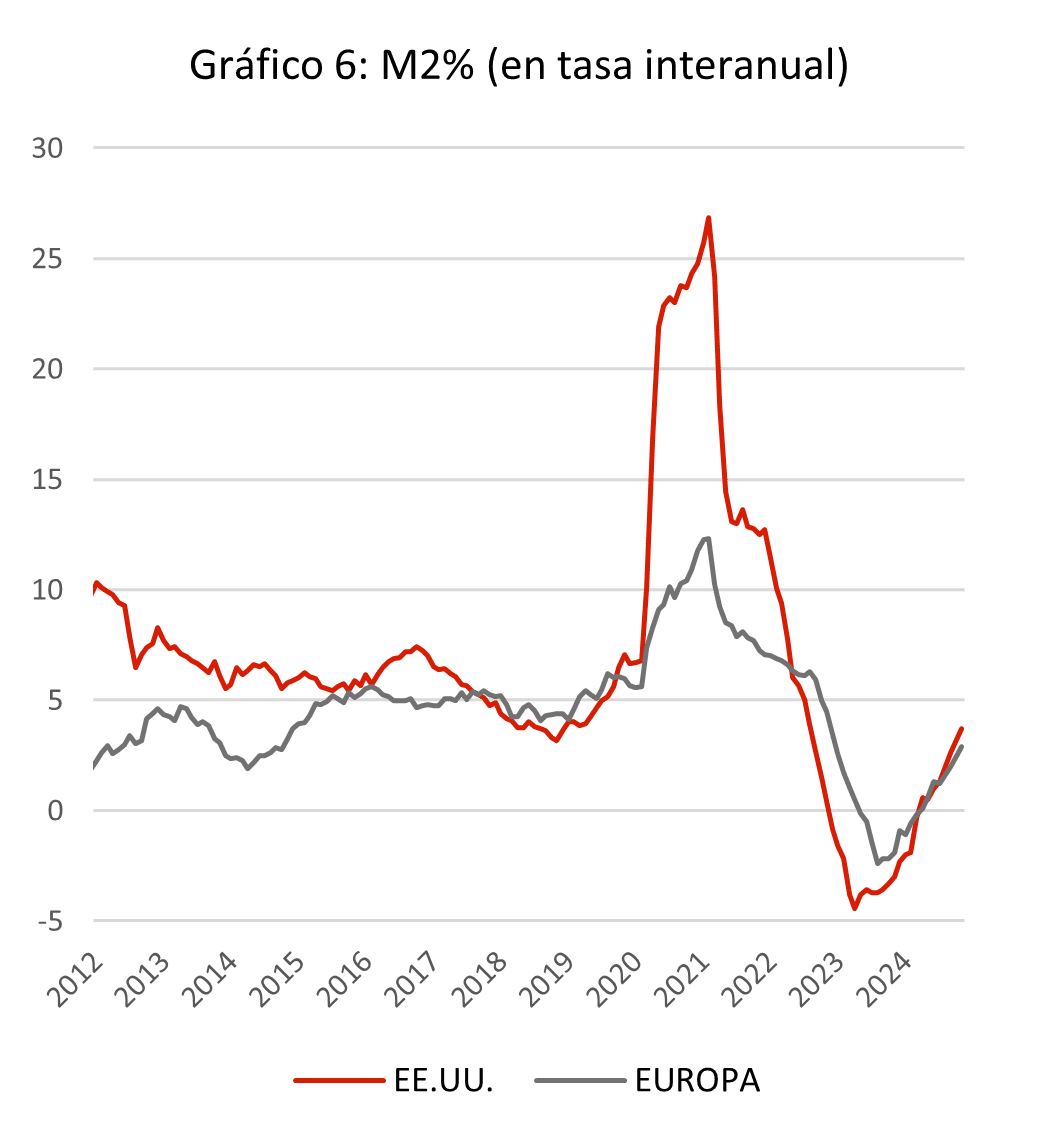

The impact of the central banks’ interest rate cuts is most evident in the real economy. Looking at M2, which includes currency in circulation and demand deposits with a maturity of up to 12 months, we’ve seen a rebound after two years of slow digestion due to the massive amount of money created in response to the pandemic (figure 6).

This may be one of the main reasons why economies have avoided recession despite rising interest rates—since the more liquidity households have, the less likely they are to cut back on consumption. If inflation doesn't spike and central banks don't have to raise interest rates again, we can expect M2 to continue to grow through 2025, possibly reaching pre-2020 levels, which would provide a tailwind for consumption.

This recovery in "real" liquidity is also a result of the easing of financial conditions for households and businesses seeking financing, driven by highly optimistic market sentiment. All indications are that this trend will continue in the coming months, although it could be quickly reversed in response to any unexpected event.

A volatile start, but reasons for optimism

The year we’ve left behind was positive in terms of returns, and there are solid reasons to expect the same from 2025. Key factors such as growth, corporate earnings, and liquidity point in this direction, with additional support from market sentiment and liquidity. Politics—both monetary and fiscal—will also play a crucial role, and not just in the United States. As we’ve already mentioned, Europe is facing a difficult situation, and the new president of the United States is unlikely to lend a helping hand.

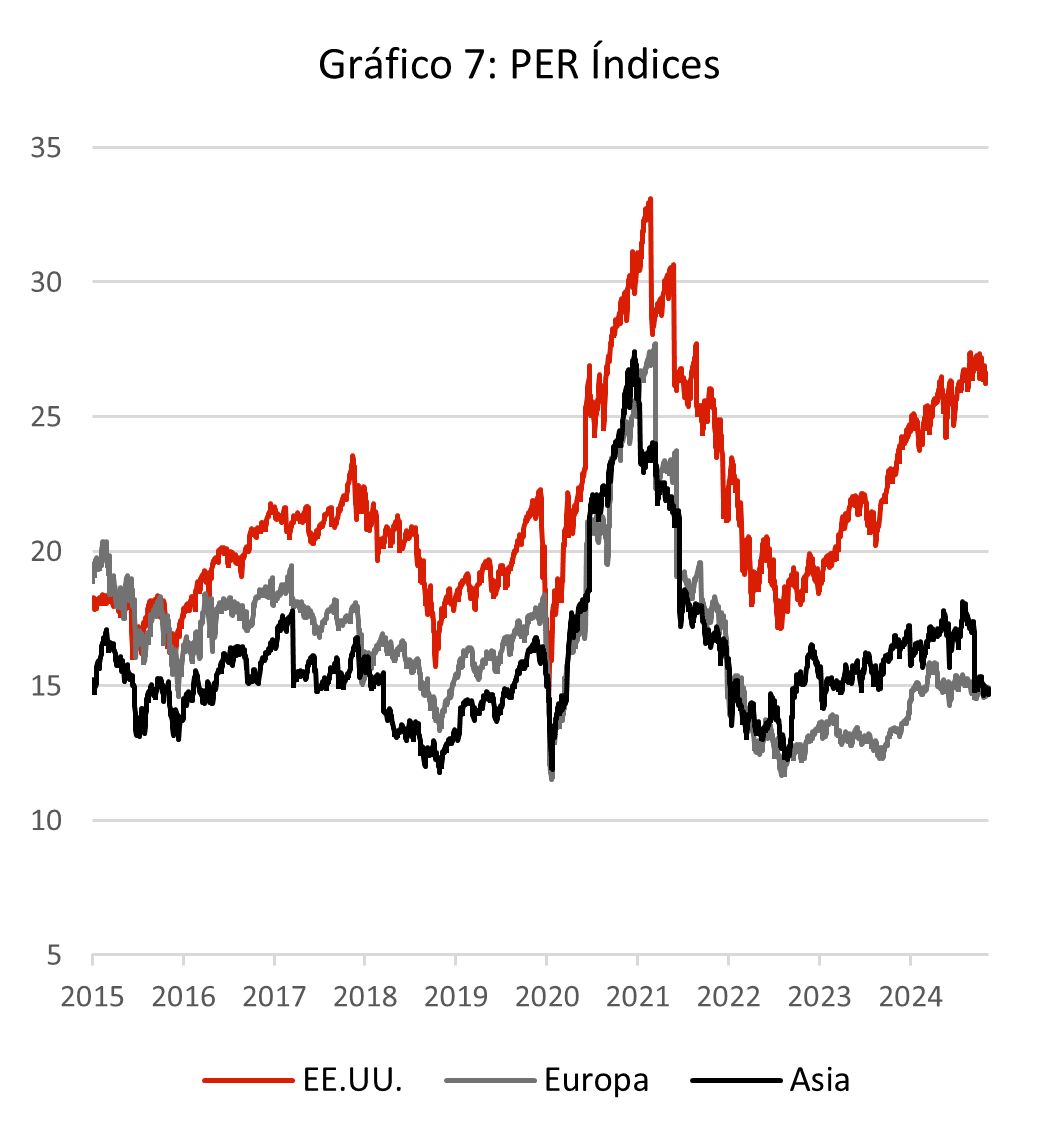

The European stock market offers more room for growth, as it benefits from some of the most attractive valuations (figure 7), and is better positioned to outperform corporate earnings growth expectations. But on the other hand, US dominance in equities appears unquestionable, so exposure to both regions needs to be managed very carefully.

The outlook for fixed income is less clear, and we recommend maintaining a neutral position. Central banks could continue to lower interest rates (pending inflationary developments), which would diminish the appeal of short-term fixed income that has previously provided a cushion of high returns.

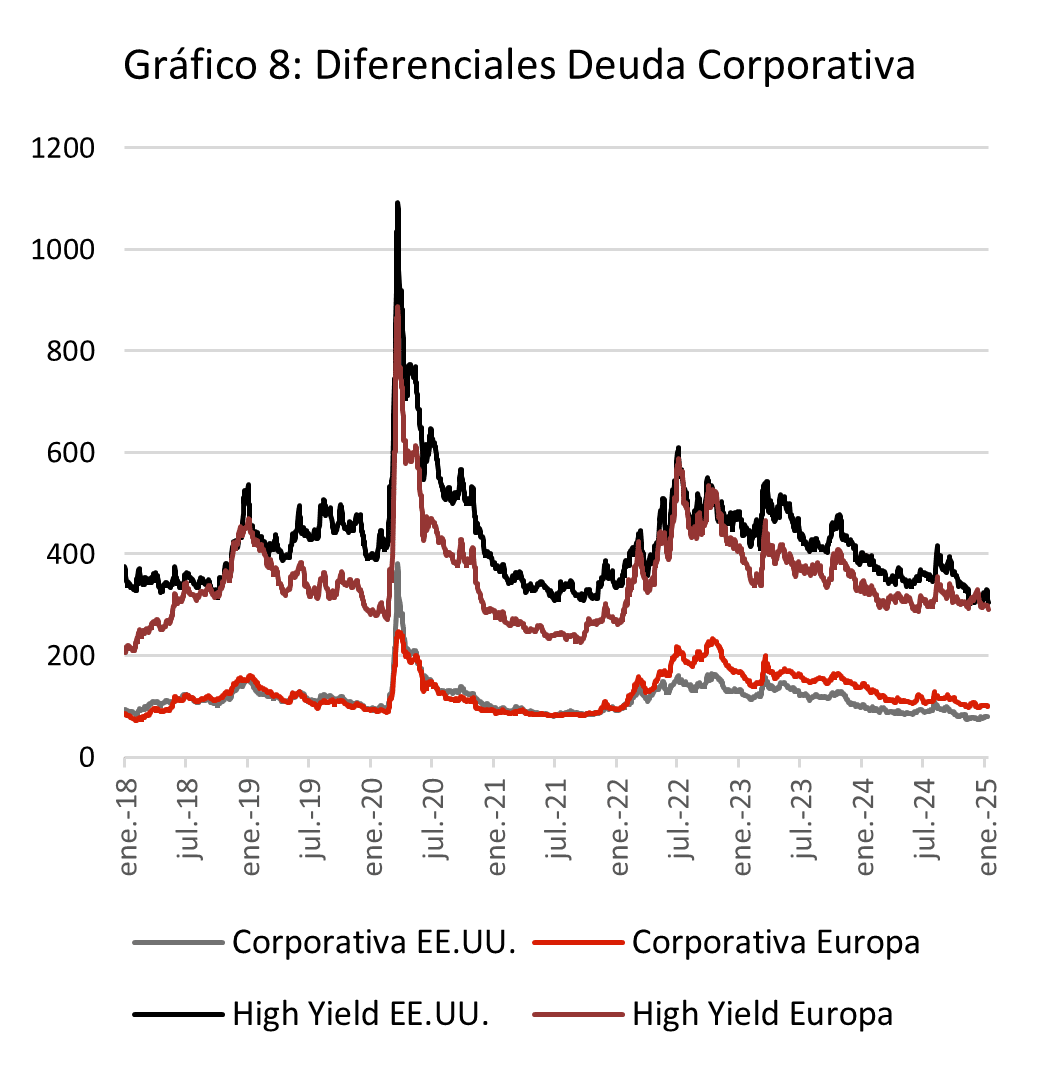

The challenge is to identify fixed income assets that offer a better risk/return profile. Government bond curves offer attractive yields following the December rebound, but volatility remains high and fiscal policy visibility is limited. If we look at corporate debt, companies’ balance sheets appear healthy, and without a recession on the horizon, they seem like an attractive asset. The problem is that much of the upside appears to be priced in, given the tightening of spreads in 2024 (figure 8). Therefore, the overall positioning remains pro-risk, despite the potential for volatility at the start of the year.