What are the economic scenarios envisaged by MAPFRE Economics?

Redacción Mapfre

Donald Trump's return to power has revolutionized the global political, economic, and commercial landscape, adding even more uncertainty to an already uncertain context. For this reason, MAPFRE Economics, MAPFRE’s research arm, has established a baseline scenario and another stressed scenario in its report “Economic and industry outlook 2025,” in the event that geopolitical tensions cause price increases, especially in energy.

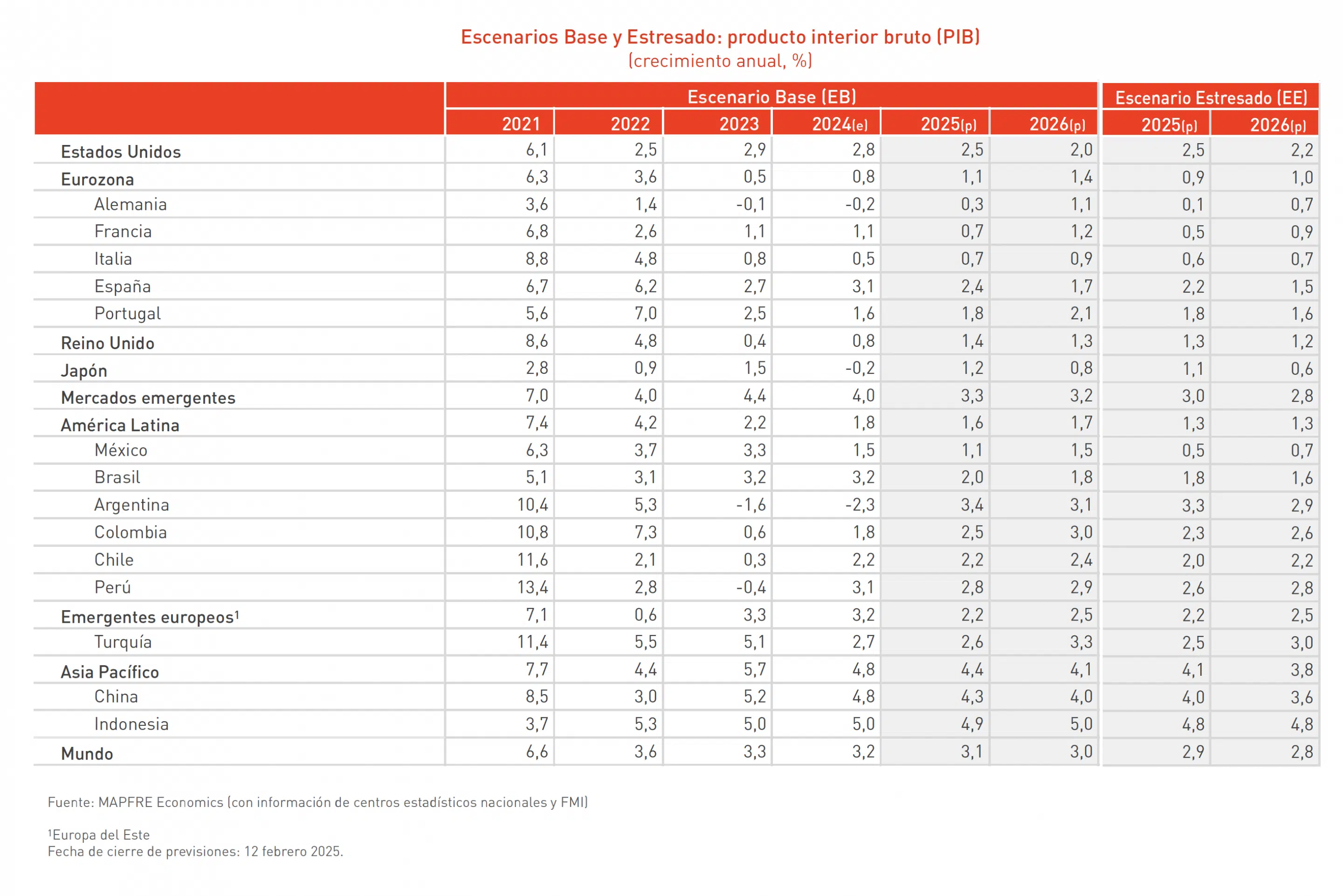

In the baseline scenario outlined in this report, global economic growth sees an improved economic outlook for 2025 and 2026 by one-tenth in each case, with growth rates of 3.1% and 3.0%, respectively, indicating that the return to potential growth remains incomplete. This slight improvement rests on marginally more positive contributions from certain developed economies, such as the Eurozone. However, the main momentum continues to come from the expansion of emerging economies, particularly in Asia, which maintains its leading contribution despite China's evident weakness.

The outlook for inflation remains on a downward trajectory in 2025, but it will continue to exceed short-term targets, averaging 3.5%. Looking ahead to 2026, a more extended horizon for global inflation control is anticipated, with a rate of 3.0%. Combined with the improved economic activity, this suggests a less stagflationary outlook compared to the past.

In terms of monetary policy, a gradual shift towards neutral policies is anticipated. However, this transition may be less orderly than in the past, when synchronized economic cycles and evident coordination facilitated a more streamlined approach.

On the other hand, the stressed scenario (a less likely alternative scenario) continues to depict a landscape dominated by geopolitical risk premiums, which are transmitted through various channels to inflation. Specifically, the source of the shock remains in energy commodities, with oil at $100 per barrel for two consecutive quarters and stable in the $90 range throughout 2025.

In this scenario, the effect on global prices rises by almost half a percentage point over the course of 2025 and 2026, while the erosion of economic activity in those two years would result in two-tenths less growth compared to the baseline scenario (2.9% and 2.8%, respectively).

For 2026, an overall worsening of half a percentage point is projected globally, as it reflects some of the lagged effects of a stricter monetary policy. Financial conditions contain an increase in tension limited to 1.5 standard deviations, with a response from risk assets similar to previous years, where the average correction is around 15% for global equities and a widening of spreads by 150 basis points. This triggers a “flight to quality,” favoring insurance and high-quality assets.

As for tariffs, a five-percentage-point increase in the general effective tariff rate of the United States is expected in 2025, which would raise the average tariff from 2-3% to 7-8%. This increase is expected to reflect a 10-15% rise in U.S. tariffs on China, as well as a response to “non-reciprocities” in tariff levels, meaning products for which a given country imposes a higher tariff than the United States. Additionally, other ad hoc tariffs on goods and trade partners are also anticipated.