U.S. supremacy in the stock market for 2025

Redacción Mapfre

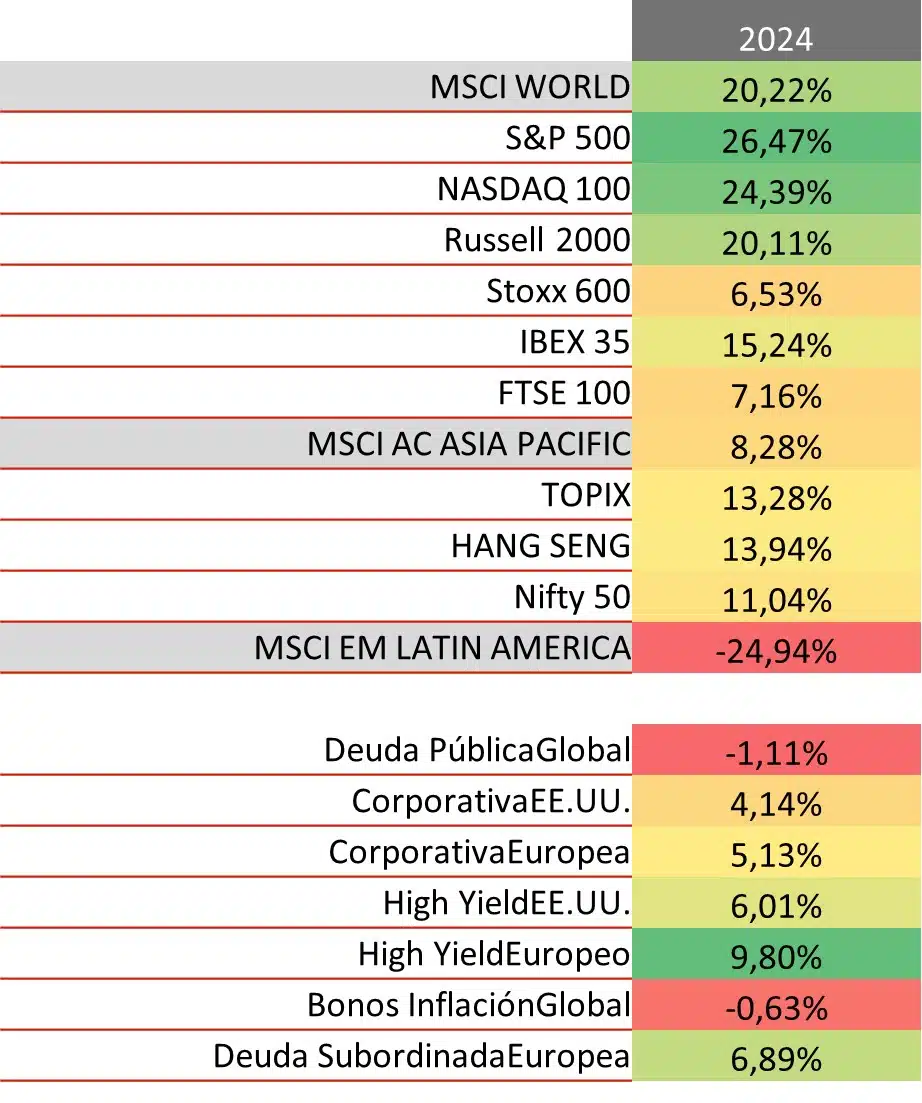

Most assets are on track to close a year of positive returns with the sole exception of Latin American equities and U.S. public debt. The outcome of the elections in the United States has not changed the overall positive market sentiment, but it has served to highlight divergences that, although recognized by a significant portion of the market, had not been as in focus for investors.

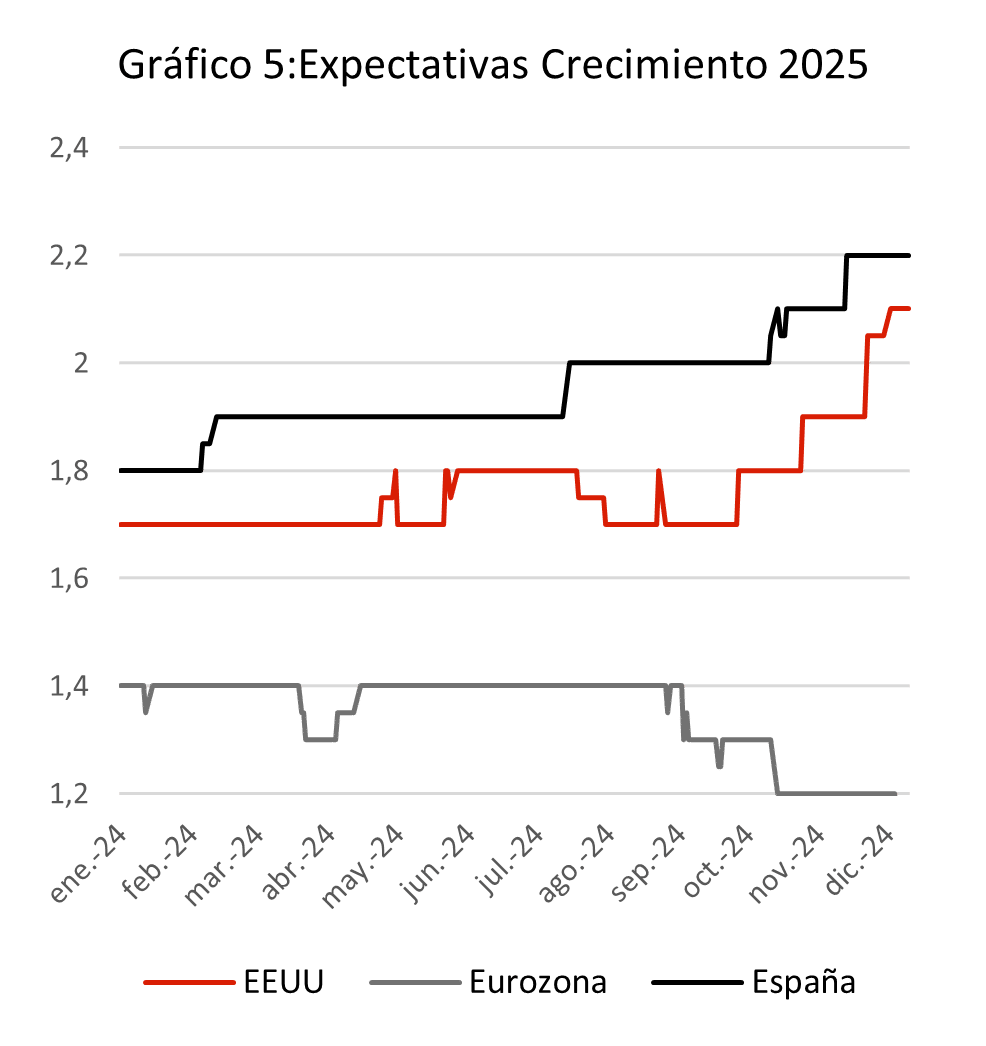

We are talking first of all about the divergence in profitability expectations for next year in European equities and U.S. equities. This is reflected in the various outlook reports for the coming year that have been published in recent weeks; some time ago, there was not so much consensus in favor of one region (United States) compared to the other (Europe). It is true that among the most respected strategists, there are conflicting opinions regarding the evolution of the S&P 500 heading into 2025 (citing demanding starting valuations and the AI boom), but none of them foresee a better relative performance for European equities.

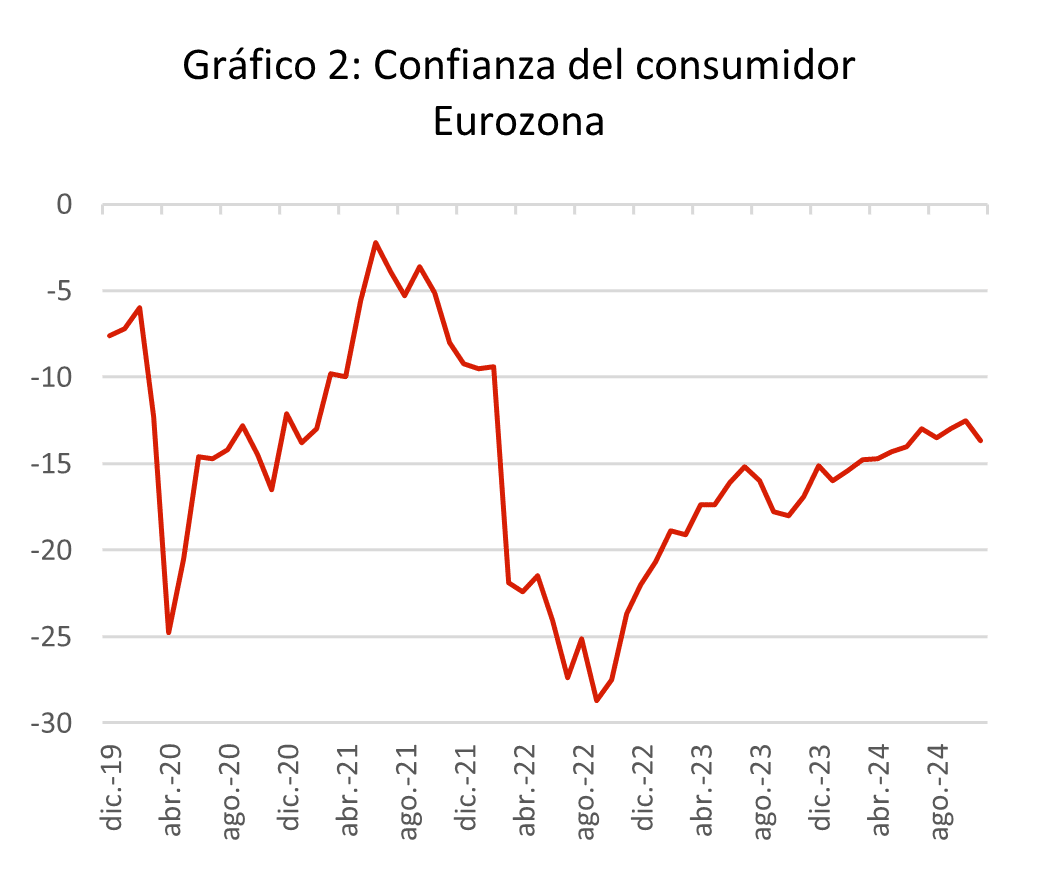

As we have mentioned on occasion, investor sentiment tends to function like a pendulum, where the shift from optimism to pessimism happens quickly. However, when it comes to the evolution of the euro area, pessimism has likely reached its extreme. And there are plenty of reasons for this: growth dynamics are disappointing, the public debt burden leaves little room for maneuver, and household confidence doesn’t suggest an increase in consumption in the future. On top of this, there is now a political situation that hinders the necessary decision-making from a structural standpoint, along with regulation that does not encourage investment in innovation. Therefore, investors' current pessimism about the euro area would be justified, but rarely, when consensus is so clear, has the market been proven right. Will this time be different?

A lot of political movement

The clear victory of Donald Trump in the presidential elections on November 5th has reduced uncertainty in the United States, as the vote count could have been prolonged for several weeks, and in that case, there was a possibility that one of the two candidates might not accept the results. With that possibility no longer in play, attention has now focused on the candidates chosen by the future President of the United States to take on such important positions as the Secretaries of State, Treasury, or Trade.

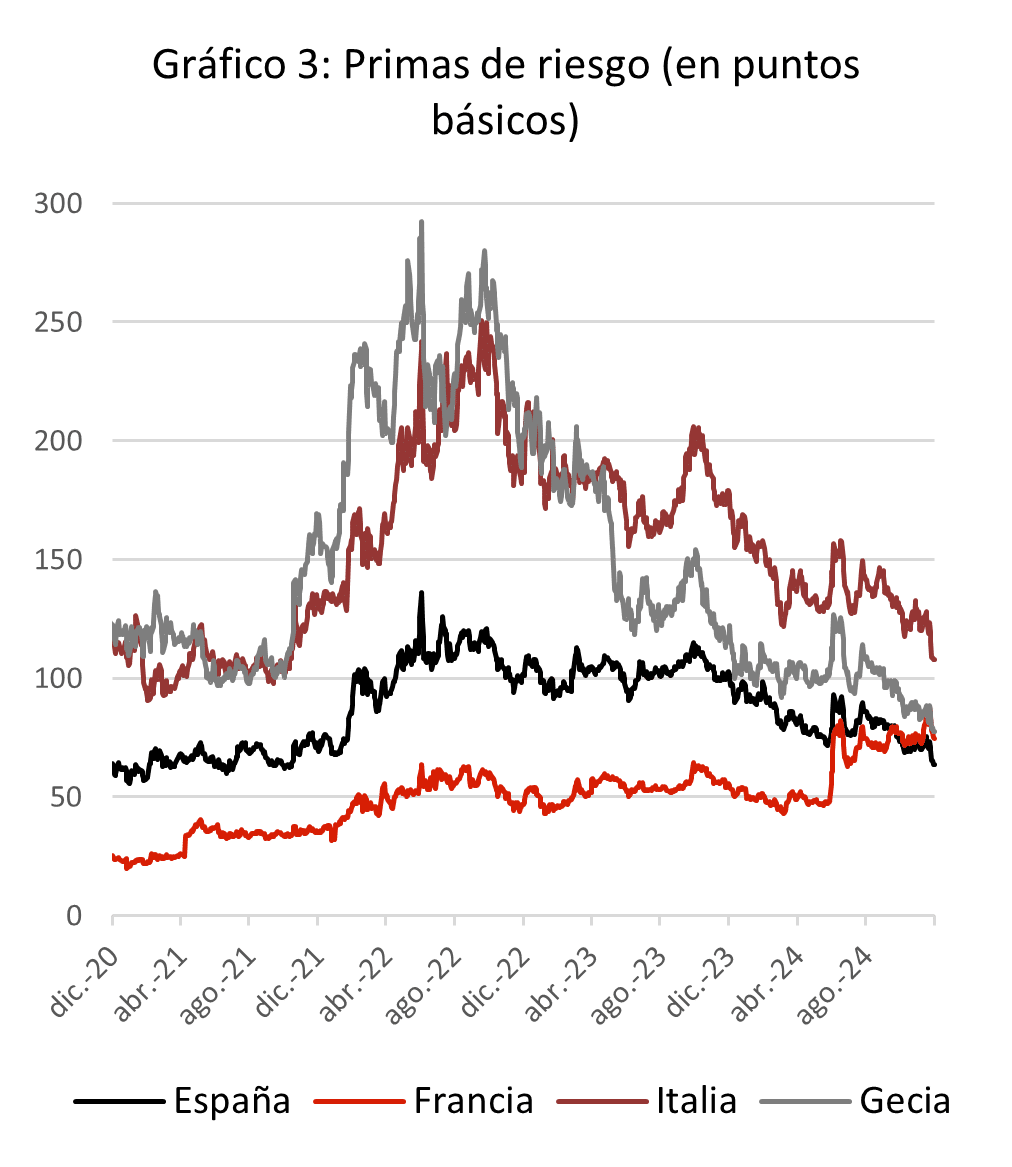

The market has been following these nominations closely, as many of the most important decisions regarding tariff policy, fiscal policy, and foreign policy will depend on them. For now, the potential candidates seem to have a more pragmatic than political approach, which has been received by the market with optimism. The polar opposite of this situation is found in France. The now former Prime Minister Michel Barnier did not pass the vote of confidence, and President Emmanuel Macron will have to nominate a new candidate, as it is not possible to call new elections until next June. This political blockade makes it very difficult to take the necessary measures to 1) fulfill the deficit reduction path that had been sent to the European Commission and 2) boost its economy.

It is true that the possibility of Barnier no longer being prime minister was largely priced in, and it did not cause any significant movements in the French risk premium. However, with this outlook, it will be difficult to see the French risk premium fall below the Spanish one in the short term.

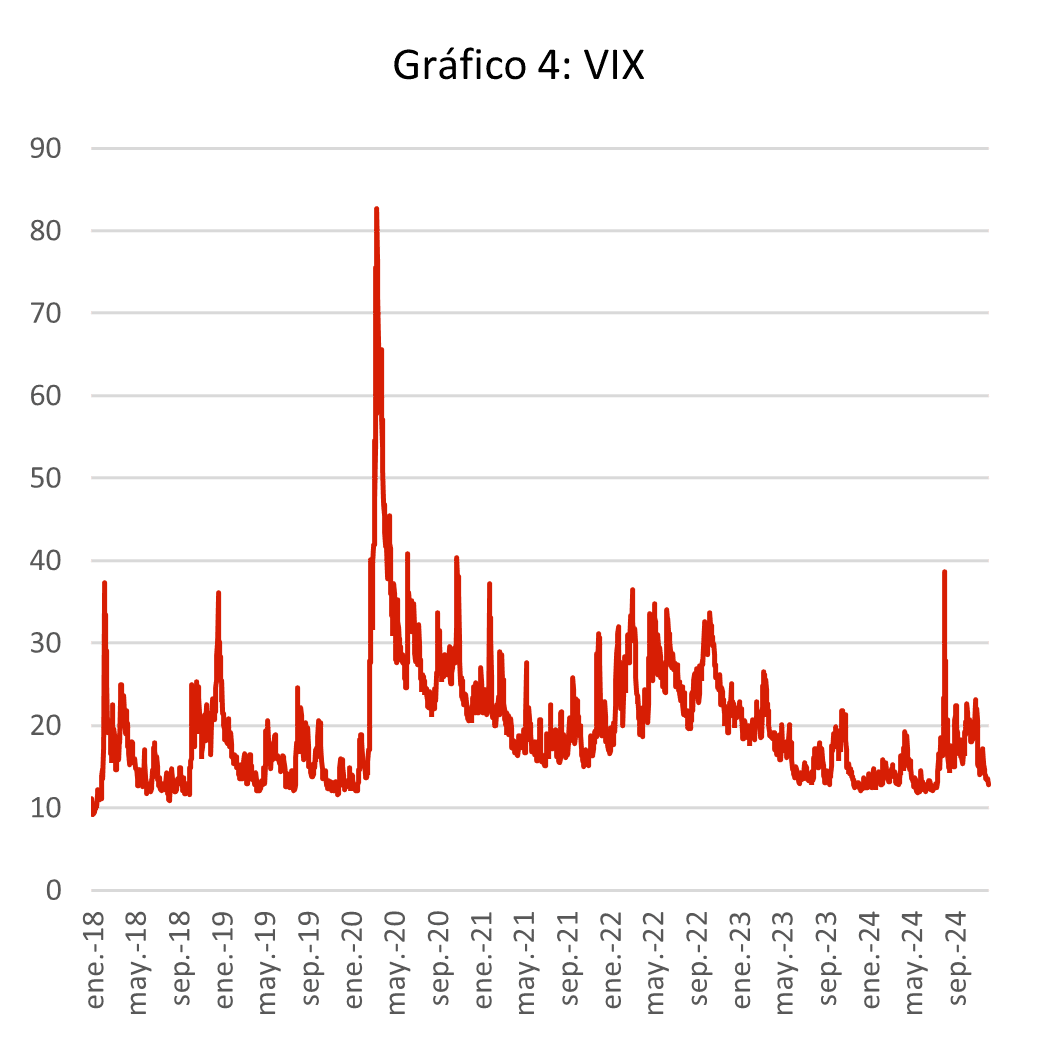

The series of political events has continued recently with the calling of elections in Germany following the breakup of the governing coalition, the more concerning episodes in South Korea and Syria, and those that remain unresolved (Russia-Ukraine, Israel-Gaza). All of this is quite complacent on the part of the markets in view of the evolution of the VIX “fear index.”

But few changes in the market

From a fundamental point of view, none of the important factors mentioned in our previous report has changed substantially. Growth dynamics continue upward in the United States and Spain and downward in the rest of the euro area. The positive reading that we can extract from the current situation is that negative sentiment can hardly go any further. The less positive reading is that it will be difficult to overcome this situation because the problems facing the Eurozone (high energy prices, poor industrial policy, competition from China, labor regulations, etc.) are of a structural nature (not circumstantial), and most of them cannot be resolved via monetary policy by lowering interest rates, as has been the case over the last decade. The solution probably involves a greater investment that stimulates economic growth, although it requires time, political will, and financing (factors that are not easy to find in the current picture).

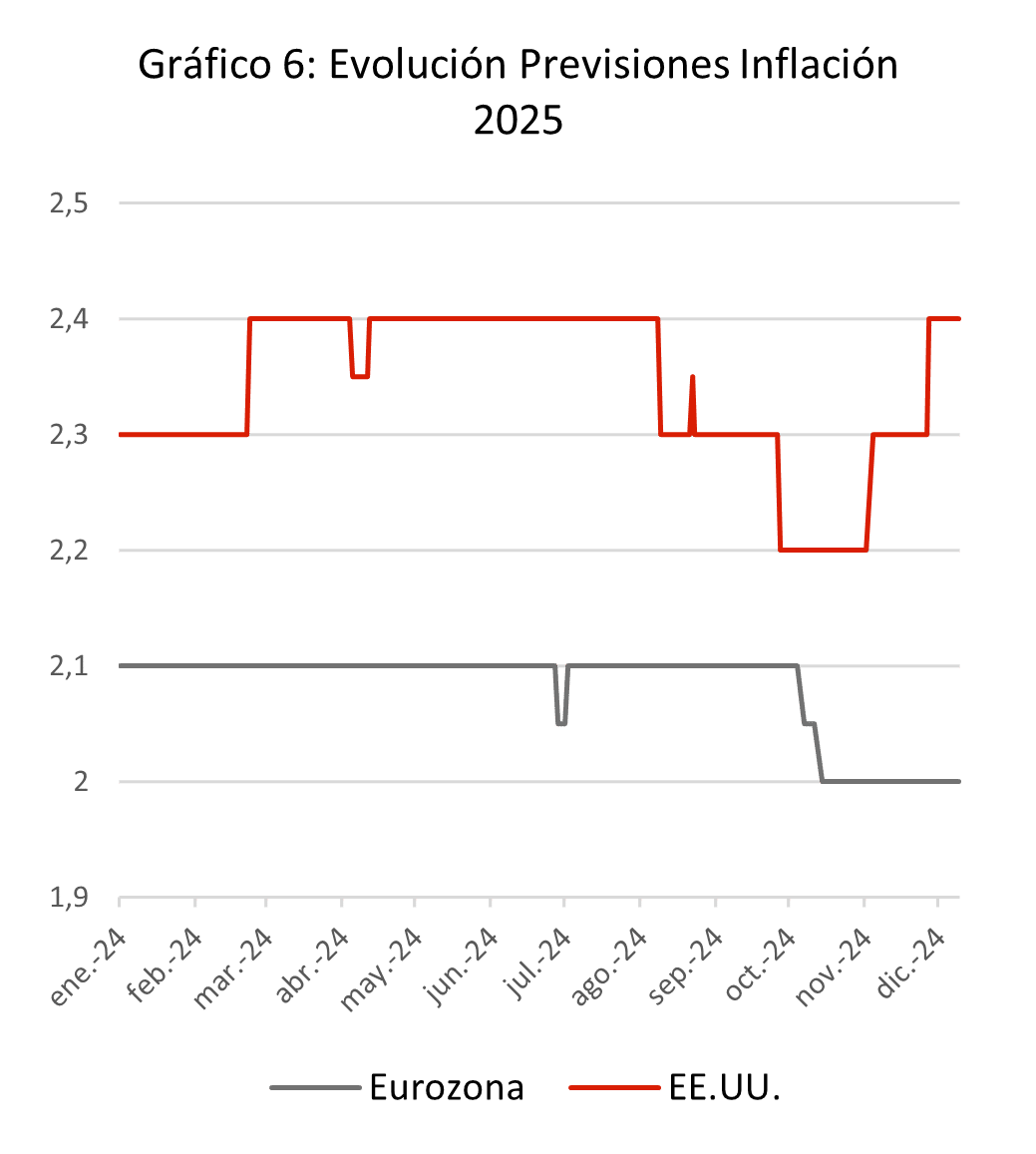

In terms of inflation, risks continue to accumulate. And again here we find a divergence in dynamics between the United States and Europe. On the European side, inflation seems to be more controlled, although it is largely due to the economic slowdown in the region and the diminishing willingness of families to consume. In contrast, the situation in the United States is totally different with growth that continues to be revised upward, a labor market that remains solid (which allows consumers to maintain their purchasing power), and a fiscal policy that will presumably generate a higher level of economic activity.

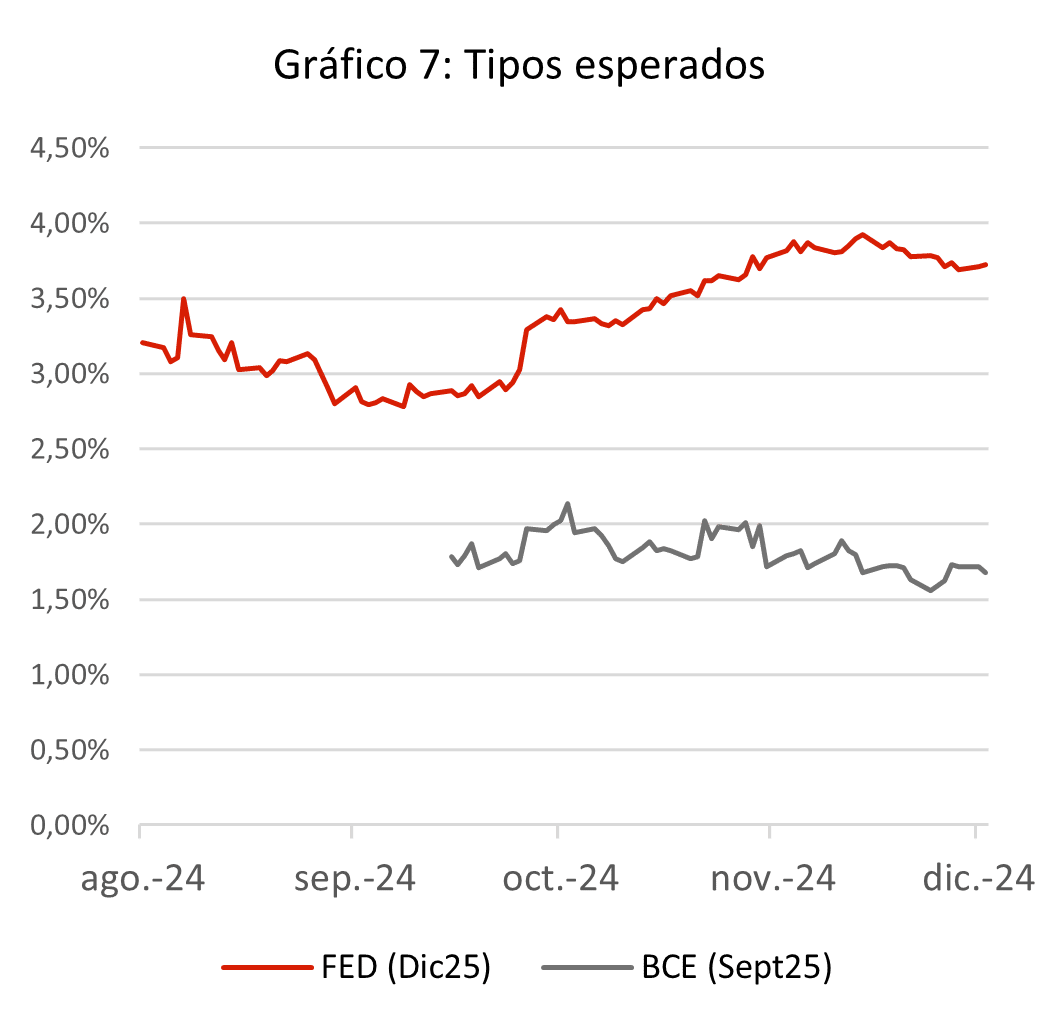

All of this is a breeding ground for inflation to move away from central bank targets, which could hamper the expectation of interest rate cuts that many investors had forecast for 2025. In this regard, the rate forecast for September next year is 1.65% for the Eurozone and 3.75% for the United States.

If we make a basic calculation in which we add expected growth to expected inflation (U.S.: 2.1% + 2.4%; Eurozone: 1.2% + 2%), the result would be much higher than the interest rate levels currently anticipated by the market in 2025. This difference is difficult to justify and should be adjusted in the short/medium term, either due to a drop in growth (unlikely) or through an increase in interest rates (more likely). This is undoubtedly a factor that will set the pace of the markets given that liquidity remains quite abundant in the market, despite central banks continuing to drain liquidity from the system.

Conclusion: American supremacy

Despite everything on the political and geopolitical front, the most important long-term dynamics for the market have not changed in recent weeks. There are well-founded reasons to believe that the good market dynamics will continue until the end of January or the beginning of February, which is usually the time when expectations are adjusted for the rest of the year based on how it has begun. The supremacy of the U.S. market is also evident, reinforced by Trump's pro-growth policies and a constant flow of money from investors attracted by the strong expected returns compared to other geographical regions.

Inflation, which could undermine hopes for a more dovish monetary policy, or a decline in the valuations of companies that have most leveraged their stock price appreciation in artificial intelligence, could serve as a counterbalance to such high optimism and consensus. Europe seems completely ruled out, but it could play a diversifying role in the event that the large companies in the S&P 500 fail to meet their business targets throughout 2025.

Finally, the measures that continue to be approved in China to promote growth could take traction over the next year and offer an attractive profitability/risk binomial given the low level of valuations from where they start. Thus, we maintain our optimism for the coming months and will need to stay very alert to the opportunities that assets outside the consensus may offer.