Trump's first month in office: “Few changes in the important things”

Redacción Mapfre

Monthly report from MAPFRE Gestión Patrimonial

We had a hunch that January would bring major headlines, as the new president of the United States had announced, after winning the election, that the first days of his term would be filled with new executive orders. Although most of his early decisions focused mainly on immigration and energy policy, we soon began to witness Donald Trump's unconventional approach to policy: build walls, but always leave a door open for negotiation. .

On the first day of February, new tariffs of up to 25% on products from Canada and Mexico would have gone into effect if not for the fact that, just hours after the news broke, President Trump and his Canadian and Mexican counterparts agreed to a one-month moratorium in exchange for increased border control by both countries to curb drug trafficking (primarily fentanyl). The initial headlines triggered a strong reaction in the market, with significant declines in equity indices and also in currencies (the Mexican peso lost 3% to the dollar), but these losses were partially mitigated after the results of the various phone calls between Trump, Justin Trudeau, and Claudia Sheinbaum became known.

Thus, there were many headlines that caused volatility in assets during the last weeks of January, but without any fundamental economic changes that would alter the long-term outlook, as the impact of tariffs remains highly uncertain. This volatility was increased by the emergence on the market of a new Chinese artificial intelligence application (DeepSeek) that could overshadow ChatGPT in terms of results obtained with a more efficient use of energy (it is estimated that up to 97% less) and that casts doubt on the huge amounts of investment that large technology companies are making in this area.

Many headlines, but few fundamental changes

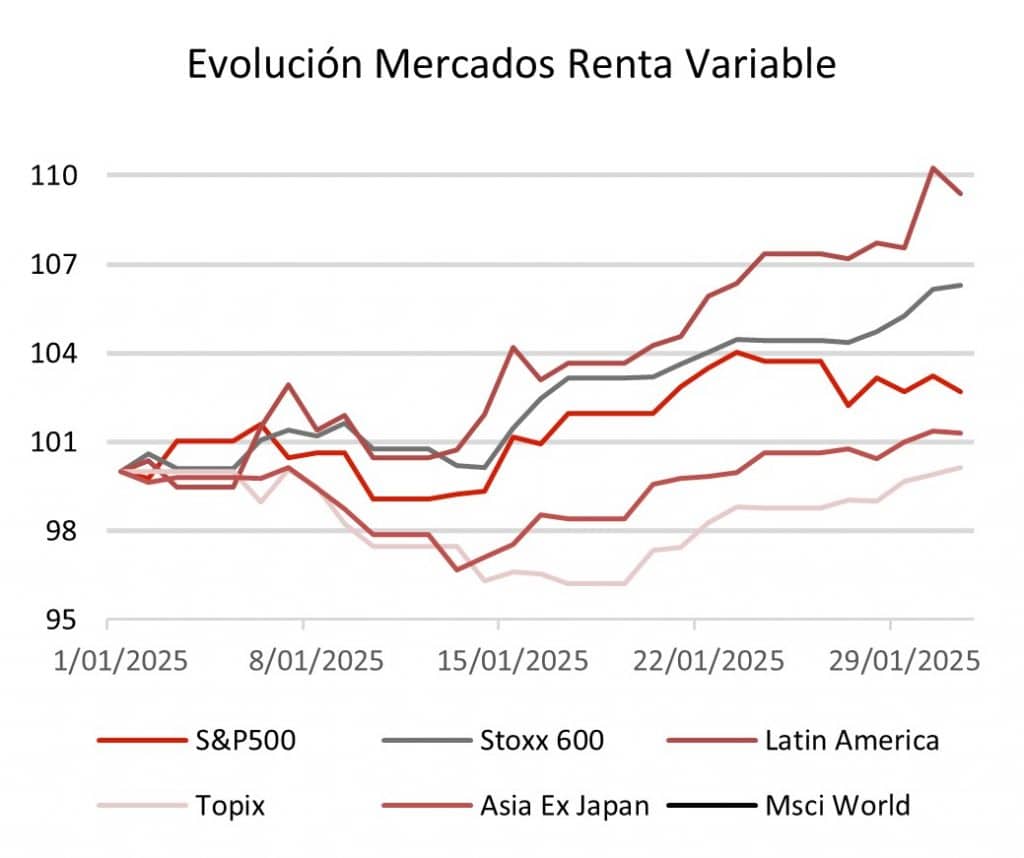

The volatility of prices for many assets in January is not supported by a substantial change in any of our five key factors (growth, inflation, liquidity, profits, and valuations). On the growth side, there have been slight improvements in the forecasts for the United States and Spain, which becomes the only country capable of following the growth path of the North American giant. Continuing with the positive surprises, the GDP outlook for the Eurozone as a whole has remained stable. Moreover, the macro surprise index has recovered significantly, approaching its neutrality level, which has allowed European stock markets to outperform their U.S. counterparts at the start of the year.

As we mentioned earlier, the market may still be uncertain about the impact of tariff impositions on growth (especially in Europe). However, the mere fact that expectations have not worsened may have been enough for investors to regain some appetite for geographically underweighted regions in portfolios, such as Latin America or Europe itself.

If we turn the focus toward Asia, we see how China started the year showing good signs of growth, but it has once again slowed down. One of the problems facing the Asian giant is that liquidity has yet to be reflected in the sentiment of households and businesses, so the multiplier effect of money creation is not having an impact. Despite this, China continues to take steps to adapt its growth model to a more domestic (less exporter), model and we have no doubt that both Trump and Xi Jinping will reach an agreement on trade since both leaders are pragmatic in their approaches.

Concern about inflation in the United States

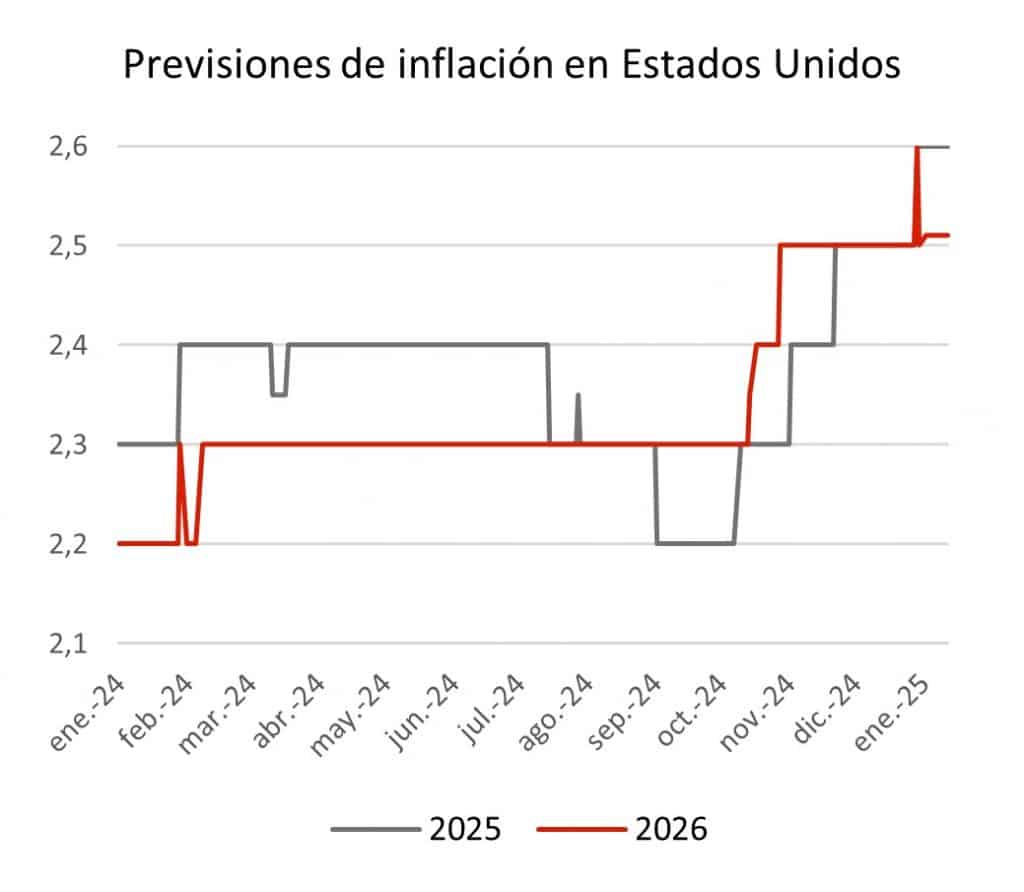

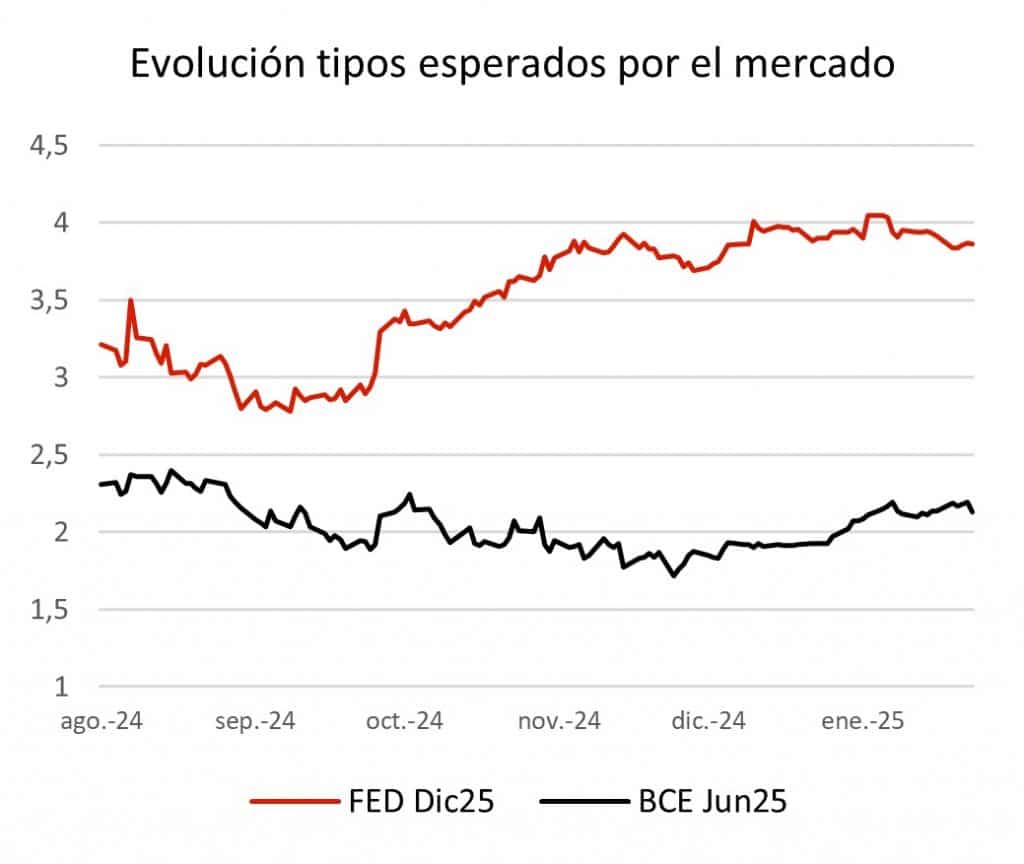

There seems to be more consensus on the impact that tariff impositions would have on inflation. Forecasts for this year and the next have been recently revised upward, which has also led the Federal Reserve (Fed) to pause further interest rate cuts. The head of U.S. monetary policy made it clear that the next move will be to lower interest rates, but not “there is an urgent need to adjust monetary policy for now.” So much so that the body's Chairman, Jerome Powell, ruled out a cut in March, and they will need several sets of downward data in order to resume cuts.

Asked about the labor market, the President of the Fed ruled out forecasting about Trump's policies, but stated that he was very attentive to immigration policy, recognizing the difficulties in some sectors when hiring personnel due to the possible reduction in migratory flows. In the case of the European Central Bank (ECB), which also made a decision on interest rates, rates were cut for the fifth consecutive time to 2.75%, and the European monetary authority stated that the disinflation process is on the “right track.” Questions will begin to arise when official rates reach 2.5%, as it would be within the upper limit of the range indicated by Christine Lagarde as a neutral rate. From then on, debates within the ECB Council will become more intense, and monetary policy decisions will be less consensual.

Linked to the recent decisions of central banks, we do not see many changes in their role as creators or destroyers of the money supply. Liquidity remains at stable levels, and financial conditions continue to be relatively loose, especially in the Eurozone, where the ECB's recent interest rate cut and the increased willingness of commercial banks to offer credit have led to an improvement in this indicator.

The earnings season is underway

In recent weeks, fourth quarter earnings have been published by the main companies on both sides of the Atlantic. U.S. banks began reporting higher earnings and revenue increases than expected, which has made them one of the best sectors in terms of profitability in January.

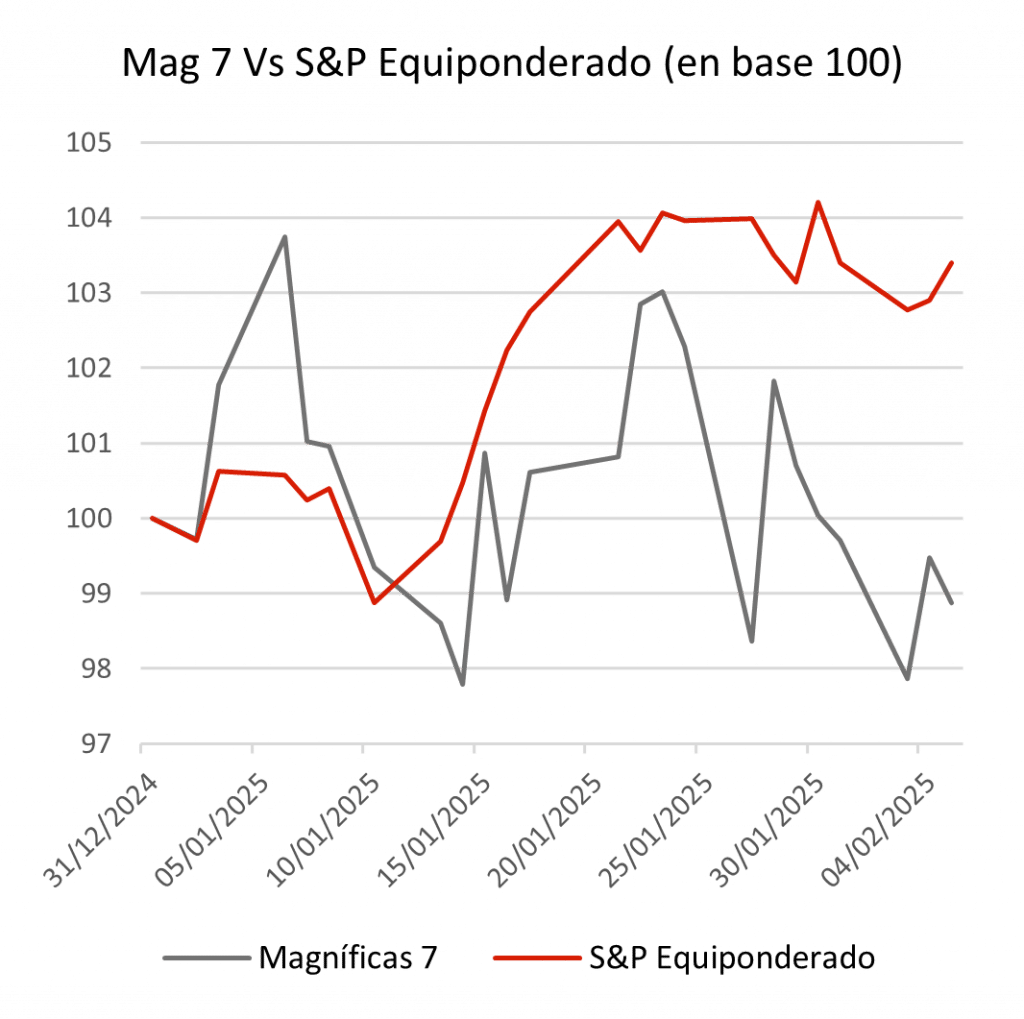

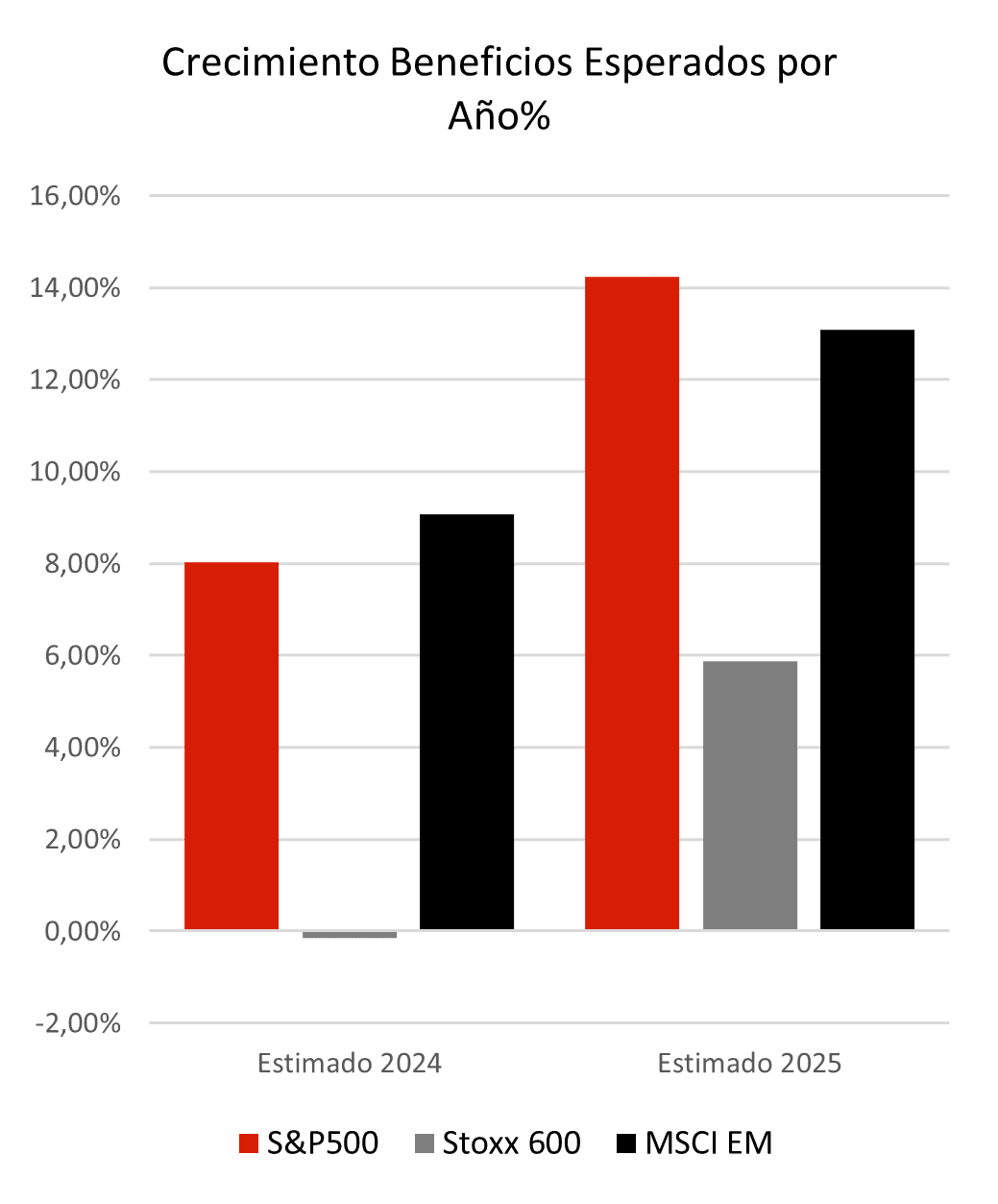

After that, it was the turn of heavyweights in the indices such as Microsoft, Meta, Alphabet, and Apple, which reported mixed results. On the positive side, Meta and Apple’s results stood out, with their stocks receiving strong boosts, while Microsoft and Alphabet were affected by cloud business growth that was lower than expected. In the case of Google's parent company, it was due to its intention to increase investment far beyond expectations over the next twelve months. By the end of January, 77% of companies that had reported earnings had exceeded expectations by an average of 5%, leading the market to now expect a 14% growth for the fourth quarter in the United States.

On the European side, the earnings season has not gained as much traction, with less than 25% of the companies in the Stoxx600 having released their results. So far, the reading is positive, with 57% of companies exceeding earnings expectations and 75% surpassing revenue expectations, with margins of 2% and 1.7%, respectively. Thus, macroeconomic uncertainty has yet to reflect on the micro level, as corporate profits still point to solid growth for 2025.

Conclusion: few changes in the important factors, but caution remains

Regarding portfolio positioning, the macro picture suggests that only minor adjustments are needed, as recent volatility may continue. However, some caution may be necessary due to the strong “growth” bias that indices and managers with more indexed portfolios have taken. The momentum factor (buying what has risen the most and selling what has fallen the most) continues to perform well, but it’s one of the worst factors when the trend unexpectedly reverses. A few months ago, it was absolutely necessary to invest large amounts of money to capitalize on AI. In just one week, DeepSeek has cast doubt on this belief, erasing over $600 billion in market capitalization from Nvidia in a single day.