¿Trump Trade or... Trap Trade?

Redacción Mapfre

Javier de Berenguer Viota, analyst and funds selector at MAPFRE Gestión Patrimonial, details in this article the potential effects that Donald Trump's policies could have on the economy and markets.

What will Trump -probably- do?

These are the main lines of action announced by Donald Trump during the election campaign.

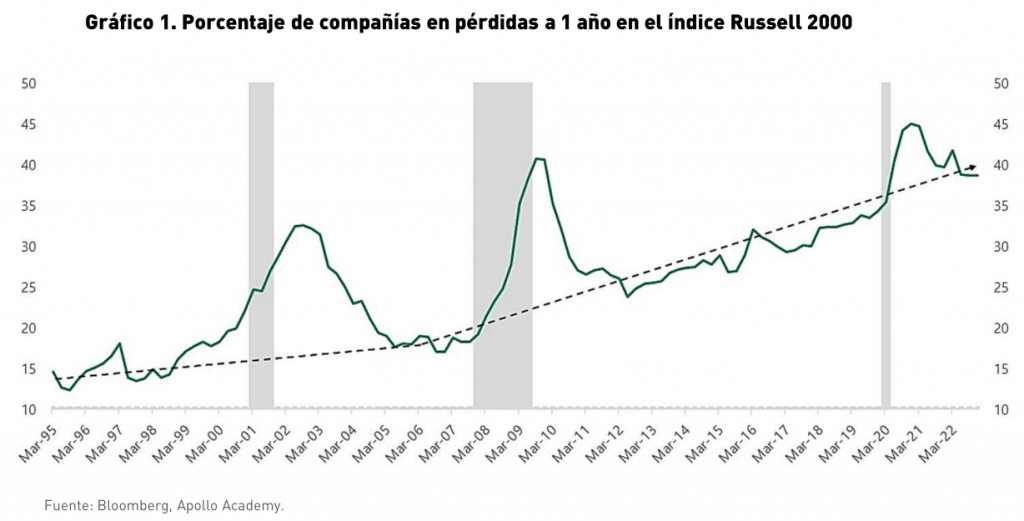

1. Corporate Tax Cut (from 21% to 15%). This measure would likely have a bullish impact on the stock market, particularly benefiting companies that rely on external factors to support their growth. However, it would not affect loss-making companies (40% of the companies in the Russell 2000 index are unprofitable, Chart 1) or companies with annual revenues below $750 million.

2. Deregulation. Deregulation directly affects industries that are heavily regulated or under scrutiny by the U.S. government. At first glance, industries such as banking, energy, technology, and small-cap companies would be the main beneficiaries. However, a more detailed analysis could reveal several complexities, which we will address later.

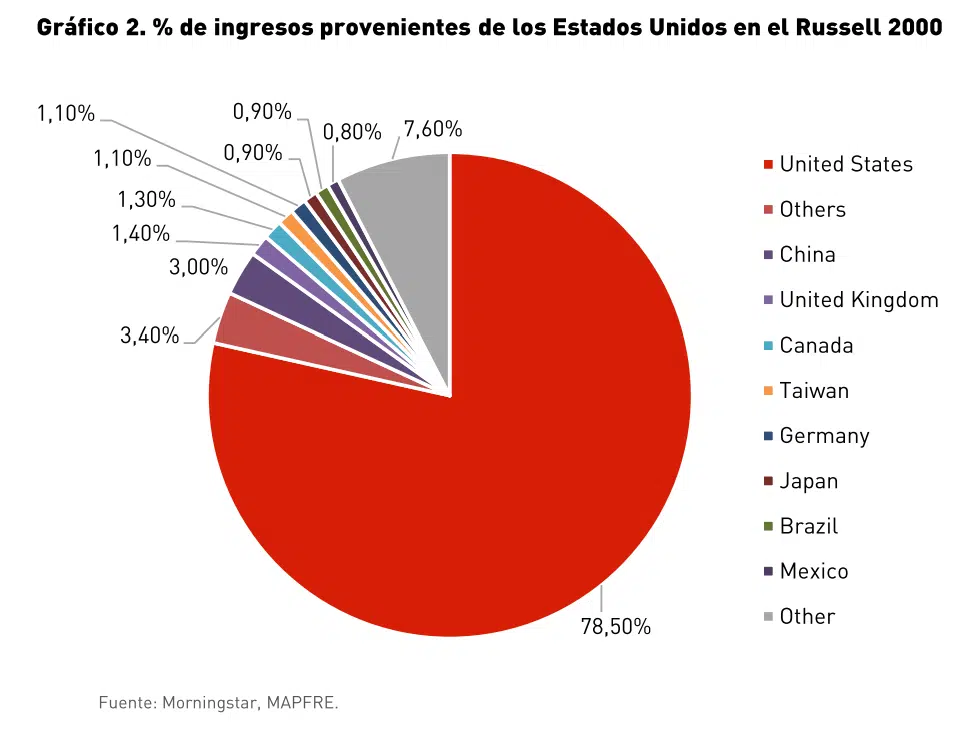

3. Higher Tariffs. Protectionist trade policies would benefit companies with higher domestic revenues. This policy is likely to be particularly advantageous for small U.S. companies (78.5% of their sales are domestic, Chart 2). However, the negative impact, which may not be immediately apparent, would fall on American companies with a large portion of their operating costs (supply chains) overseas, especially those reliant on Chinese manufacturing. We don’t expect these measures to be implemented immediately but rather to be used as bargaining leverage for better trade deals, with gradual implementation over time.

4. Immigration. The President’s plans for mass deportations and restrictions on legal immigration would result in significant economic costs with minimal or no benefits. This policy is considered to be the most ideologically driven in Donald Trump’s agenda. Industries with high foreign labor input, such as construction, hospitality, and agriculture, would face labor shortages, leading to reduced production and higher labor costs.

5. Expansion of the Fiscal Deficit. Rather than being a direct policy (no candidate campaigns on increasing national debt), this is more a consequence of the measures mentioned above. Only the tariff increases would theoretically boost fiscal revenue, but this would be limited, as many of the country’s imports have highly elastic demand, meaning consumers would reduce purchases if prices rise. Other policies would likely lead to lower fiscal revenue overall. Trump has already hinted at the impact of these policies and his plans for offsetting them, such as influencing Fed interest rate decisions or pushing for Bitcoin to become a reserve currency.

Pros and Cons in the Markets.

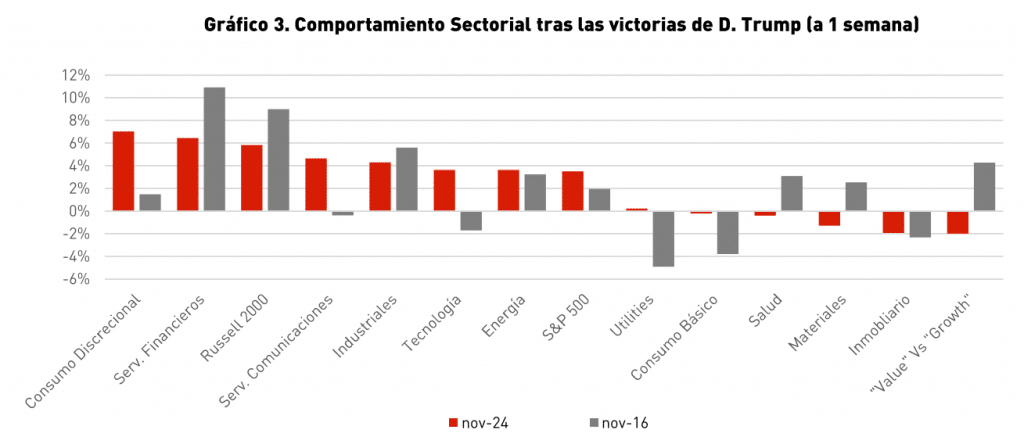

At the sector level, impacts vary in magnitude and timeframe:

a) Energy: This sector has been identified as a “winner” with the return of Donald Trump (+3.62%, one week post-election), specifically traditional energy. This is due to the “positive” effects of deregulation (greater freedom to produce) and a less favorable administration toward clean energy (fewer subsidies = higher costs = reduced competitiveness). However, despite the clear short-term benefits for traditional energy producers, these measures could increase competition (via fracking), leading to lower operating margins (lower prices as a result of higher volume and competition). In other words, while established companies might initially benefit from increased production, over the medium term, new competitors could erode margins, reducing profits.

b) Technology: Another sector identified as a “winner” after the election, mainly due to expectations of a less confrontational stance toward the monopolistic behavior of major companies in the sector (though this remains to be seen). More evident is the likely adoption of aggressive trade policies against China and its tech companies. However, it’s important to note that many of the large U.S. tech firms are deeply interconnected with the Chinese market (through manufacturing, revenues, etc.), making it necessary to assess the impact case by case within the sector.

c) Financial: Arguably the biggest beneficiary, at least from our perspective. Although we typically avoid basing investments on speculative events like presidential elections, there are reasons for optimism. The first is deregulation, which is unequivocally positive, especially in the short term, driving higher transaction volumes (increased M&A activity, reduced capital requirements). The second—and most important—is the impact of growth, inflation, and deficit-driven policies, which are expected to push interest rates higher, expanding net interest margins—banks’ primary profit driver. Among financial companies, life insurance companies stand out, as they could benefit the most from rising inflation and interest rates while facing lower cyclical risks (less exposure to potential secondary effects like increased loan defaults).

d) Real Estate: This sector is one of the losers post-election. The reasons include reduced labor availability and the likelihood of higher mortgage rates, both of which would hinder the sector’s performance in the coming years.

e) Discretionary Consumption: This sector comprises a wide variety of companies with notable differences.. Initially, firms with a higher percentage of domestic sales could benefit from stronger growth momentum. However, this effect would need to be supported by brand strength to counterbalance cost increases resulting from higher inflation and interest rates.

f) Industrial: Another theoretical “winner”, based on increased tariffs. Additionally, the sector stands to gain from higher domestic energy production (lower costs) and increased government investments. This includes the potential realization of “reshoring” (relocating manufacturing back to the U.S.), a longstanding goal of Donald Trump that may be prioritized during his administration.

g) Defensive Sectors: While these industries encompass diverse segments, the current risk-on environment does not favor them. What’s more, many defensive sectors are burdened by higher financial costs due to their elevated debt levels. However, their defensive role during downturns, combined with uncertainties around the longer-term effects of Trump’s policies, makes them a solid complementary option for portfolios.

Our view on the "Trump Trade"

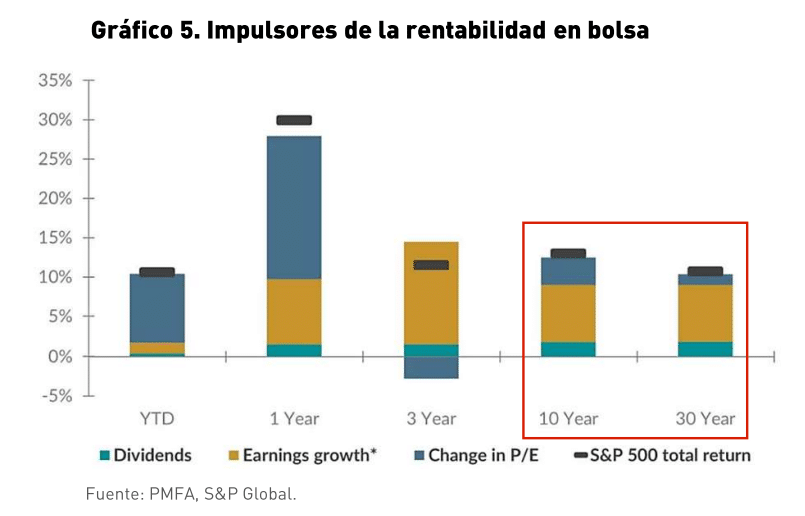

To form a well-founded position, it’s essential to move beyond surface-level perceptions and conduct a deeper analysis. In our view, the more complex, less apparent implications are what truly matter—the “important” factors. In contrast, the widely discussed and obvious implications are what we refer to as “interesting”. Ultimately, what drives markets and stock prices are future earnings (see Chart 5). To confidently invest in a specific sector or company, there must be a clear and positive link between the announced policies and the projected growth in profit. Conversely, the “interesting” aspects often dominate headlines, focusing more on market sentiment than concrete financial outcomes.

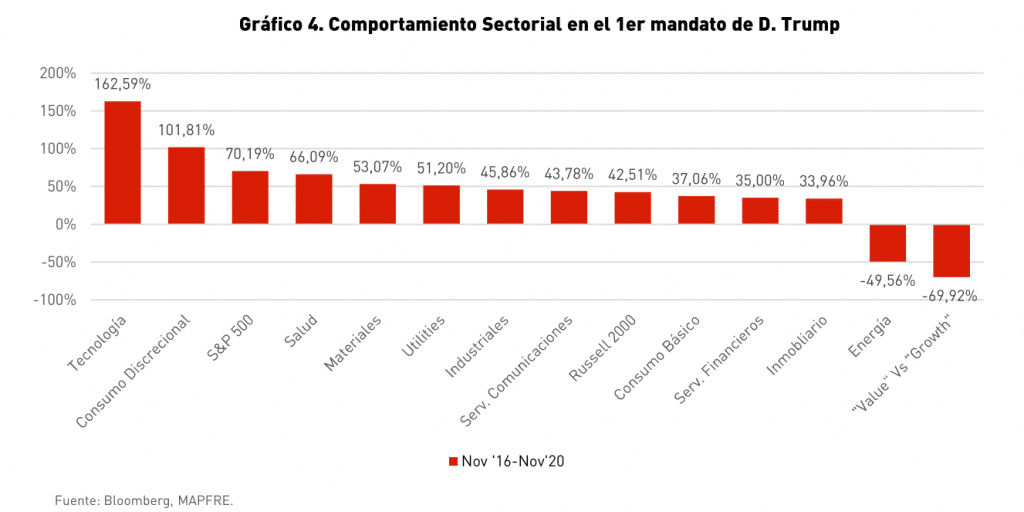

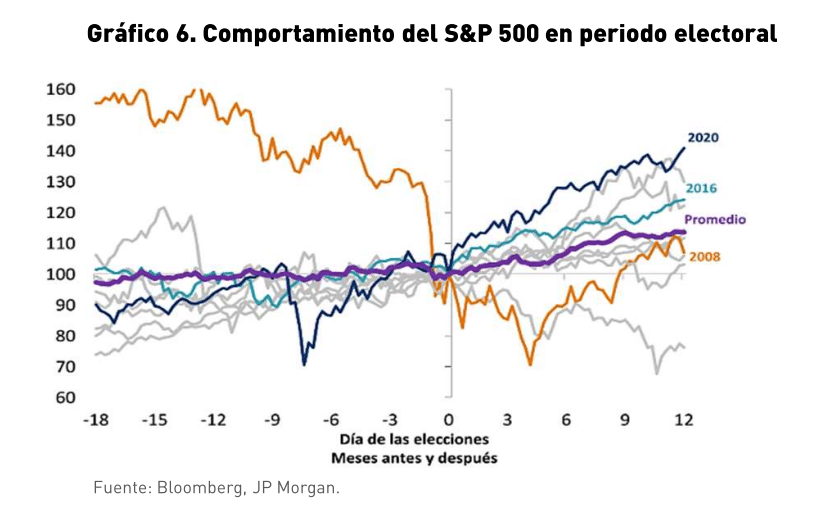

As long-term portfolio managers, we cannot afford to be influenced by what is merely interesting. Recent market developments follow a familiar pattern: once uncertainty is resolved, markets typically react positively (see Chart 6). However, this time, the context behind the bullish reaction in the U.S. market is unique. It stems from a starting point characterized by high valuations, low or even negative equity risk premiums, fiscal challenges, and an economy already growing above its potential. This backdrop leads us to believe that Trump’s influence on the markets in the short term may be more limited than it was in 2016.

We understand the reaction of the indices to some degree. Markets had positioned themselves for a divided government (House and Senate) and were instead surprised by the decisive victory of a more “liberal” candidate. Even so, if the proposed measures are implemented, they are likely to have both positive and negative effects—some clear and others more ambiguous. This reinforces our focus on company fundamentals as the primary driver of long-term profitability.