Three things you need to know in 2024 that could move markets

Redacción Mapfre

While 2023 closed as the year in which the U.S. and global economic recession was weathered, equities had a spectacular year. The S&P 500, reference index of the United States stock exchange, climbed more than 21%, while the Eurostoxx 50, which groups the 50 most important companies in the Eurozone, closed with a 16% increase. The question know is what dynamics can be mapped out, and how investors can take advantage of them.

It is a complex puzzle. The macroeconomy, on one hand, is constantly threatening a slowdown. And the markets, on the other hand. In the United States, the market consensus forecasts a more than 11% increase in profits for the companies that make up the S&P 500 index in 2024, according to data compiled by FactSet.

This increase would amount to 6.3% in the case of developed markets, excluding the United States and including the European Union, and 18% in emerging markets. As 2023 was a challenging year, some market participants see a possible earnings rebound this year as a logical outcome, which would provide some upside for the equity market.

But there are certain risks that could cause a significant revision in the profit forecast, which include the possible slowing of consumption given persistent inflation, slowing economic growth in Europe and China, and the expanding geopolitical risk caused by the conflicts in Ukraine and Israel.

These are broad-brush events. However, there are a number of catalysts to keep in mind during 2024 that could have a significant impact on stock prices.

Elections in the United States this year could move the market

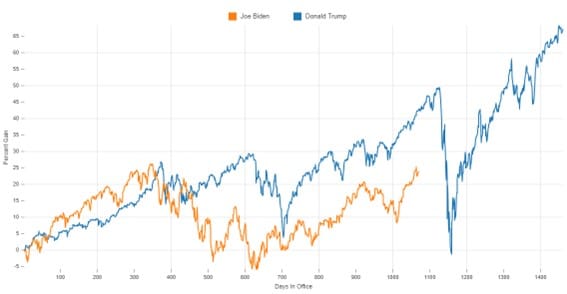

Next November, the United States will hold presidential elections. Today, everything seems to indicate that Joe Biden, the country's current president, will again face Donald Trump, the former president from 2016 to 2020. The polls are certainly tight, although somewhat favorable to the potential Republican candidate with more than a 3.8% margin, according to Real Clear Politics data.

The agendas of the two aspirants could undoubtedly have an impact on market behavior, as has occurred at other times in history. Seasonality in the stock market tends to accelerate favorably as the election approaches. But as the race nears, Wall Street's average returns are 1.7%, lower than non-election cycles.

Also, how does Trump compare to Biden on the stock market, and vice versa? Cumulatively, Trump has a 43.13% return on the S&P 500 versus Biden's 23.99%, with data at the close of 2023, a 19.14% difference. On the Nasdaq, Trump has a 62.57% yield versus Biden's 12.07%, a 50.50% difference. Finally, on the Dow Jones, Trump scores 45.17% versus 20.58%, a 24.59% difference. This statistic must be considered for the coming cycle in terms of the stock market.

Biden vs. Trump on the SP500. Source: Facts First

Debt refinancing could affect stock prices

One factor that could add volatility has to do with debt refinancing by U.S. Companies and the American government. Some of the largest Wall Street companies face billions of dollars in additional interest costs and hits on their profits if they refinance their 2024 maturities at current rates, as one third of them lack the cash to repay the upcoming debt.

Non-financial S&P 500 companies have a combined debt of 107.700 billion dollars which matures this year, at an average interest rate of 2.8%, according to a Calcbench analysis. Refinancing at greater than 5%, the current 1-year Treasury bill rate, would add another 3.090 billion dollars in collective interest expense, according to this analysis.

This is another source of concern to consider in 2024. A recent JP Morgan study warns of how regional banks could get into trouble in the markets due to their bond portfolios: Some 22 banks with between 10 and 100 billion in assets hold commercial real estate loans three times greater than their capital. Among the companies with less than 10 billion dollars in assets, 47 have huge portfolios. This could cause problems if issues and balances are not cleaned up.

And who profits from this? According to the Economic and industry outlook and updates report published by MAPFRE Economics, MAPFRE’s research arm: “The high levels of interest rates compared to the last decade, as well as expectations that rates may continue to drop, will continue to favor the savings-linked Life insurance.”

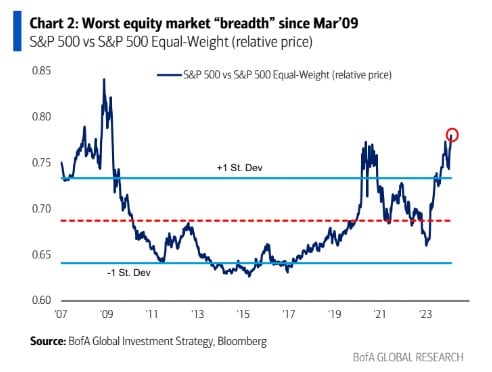

Risk of market breadth

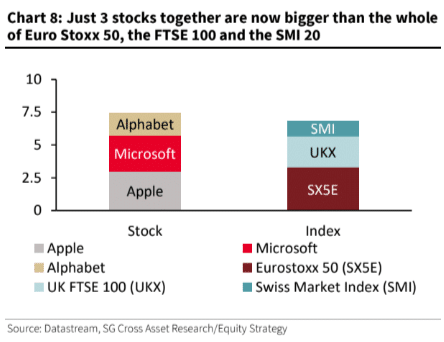

Another factor that could be a drawback in the future has to do with the concentration of stocks within the S&P 500. That is, the U.S. Stock Exchange is over-represented by companies with much higher market capitalization: Google, Meta, Amazon, Nvidia, Microsoft, Tesla and Apple.

The dimension is such that Alphabet, Microsoft and Apple exceed the market of the United Kingdom Stock Market, the Swiss Stock Market and the Eurostoxx 50, combined, in capitalization.

The current market breadth is the worst since 2009. According to Bank of America, this may pose "risks" going forward, considering that the upward movement has been driven mainly by companies with much larger market capitalization.