The ripple effect of Trump's actions continues, but there's no need to panic

Redacción Mapfre

The geopolitical order has been upended over the past month, creating ripples across asset classes much like a stone dropped into a pond. Trump's foreign policy decisions have had far-reaching impacts that have left no one untouched.

On the tariff front, the US President announced 25% tariffs on Mexico and Canada and 10% on China (later increased to 20%), which are set to take effect in March. These measures are expected to disrupt supply chains across numerous industries, given the importance of both countries in US trade.

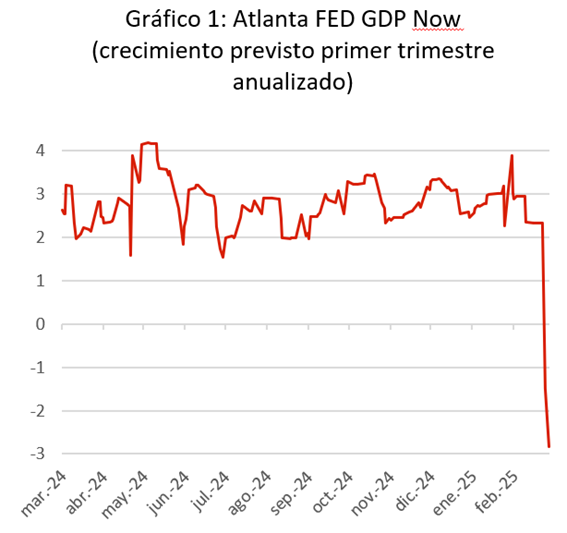

The prevailing view in the debate over the inflationary impact of these tariffs is that they will raise the prices of the affected goods in the short term, with consumers ultimately bearing the cost. However, considering the scale of the tariffs and potential retaliatory measures from Canada and Mexico, the most pronounced effect has been diminished confidence in the future trajectory of the US economy. The Atlanta Fed's GDPNow indicator, which provides near real-time monitoring of US growth, has seen projections plummet from 2.5% to -2.8% in just a few weeks (Chart 1).

Weaker-than-expected economic data, coupled with the uncertainty and mistrust generated by Trump’s policies, have raised doubts about American "exceptionalism" for the first time in years. As a result, assets that initially benefited most from Trump’s election have reversed course. The ripple effect of the tariff wave is also being felt in Europe, which is already bracing for new tariffs set to take effect in April. Last but not least, the withdrawal of aid to Ukraine has prompted European leaders to search for the right solution to maintain military support.

Growth may decline...

The approach that Trump is taking with his economic policy is the opposite of what he did in his first term. In 2016, he began his presidency with tax cuts and deregulation, which boosted the US economy before he later pivoted to a trade war, mainly with China.

This time, the least growth-friendly measures (tariffs, deportation of undocumented workers, and reduced fiscal spending) are coming before his promised tax cuts and deregulation meant to help companies set up shop in the United States. The sharp decline in American consumer confidence is thus hardly surprising, given that they voted in the November elections for a president they thought would stop the eroding purchasing power caused by inflation under the Biden administration.

US growth forecasts have barely changed in recent weeks, as uncertainty remains so high that any prediction could quickly become outdated with a single headline. This stands in stark contrast to the Atlanta Fed index mentioned earlier.

What's important in this case is that the sharp decline is driven entirely by the external sector (a steep drop in net exports) and not by significant damage to domestic demand. This is precisely where the biggest risk lies: if falling consumer confidence translates into increased saving and reduced consumption, we're likely to see downward revisions to growth forecasts.

In Europe, expected growth remains very low, despite the German election results and the response from European governments to increase defense spending, which have helped European indices diverge (this time in a positive direction) from their North American counterparts.

While it’s true that Germany's abandonment of fiscal discipline represents a major paradigm shift, defense spending has a very low multiplier effect on GDP, and infrastructure spending will take considerable time to make an impact. That said, the positive takeaway is that European growth seems to have bottomed out, and European leaders have shown increased willingness to pull Europe out of its period of sluggish growth.

...and inflation concerns persist

In recent weeks, inflation has taken a back seat to the constant stream of headlines, but it remains the most pressing risk in our view. Tariffs pose a challenge to central banks because the inflation they generate can't be addressed with conventional monetary policy tools.

Nevertheless, growing doubts about US growth have been enough to prompt the market to price in as many as three Fed rate cuts in 2025, a significant shift from the single cut initially expected at the start of the year. In Europe, higher fiscal spending is putting pressure on interest rates, so it will be important to monitor the ECB's response to these spending plans.

Endogenous liquidity under pressure

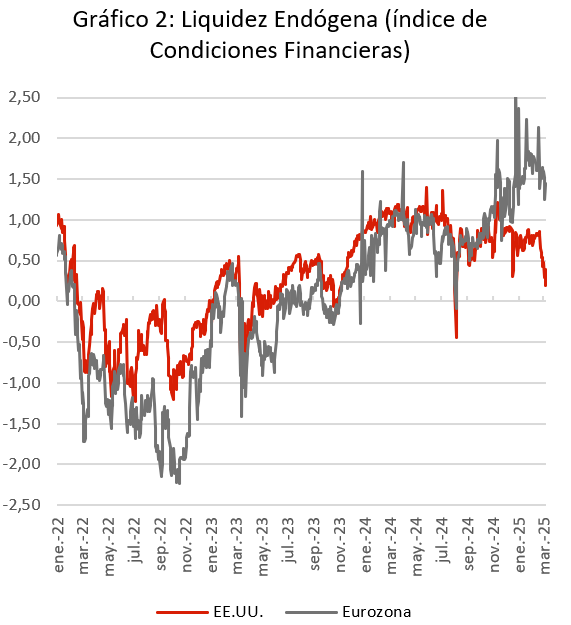

In these market updates, we regularly discuss a critical factor for financial assets: liquidity. We always distinguish between exogenous liquidity (provided by central banks) and endogenous liquidity (generated by the market itself), as they follow very different dynamics.

This time, we want to focus on the Financial Conditions Index, as it's the most reliable indicator for tracking endogenous liquidity. Looking at chart 2, this index has fallen significantly, especially in the United States over recent weeks.

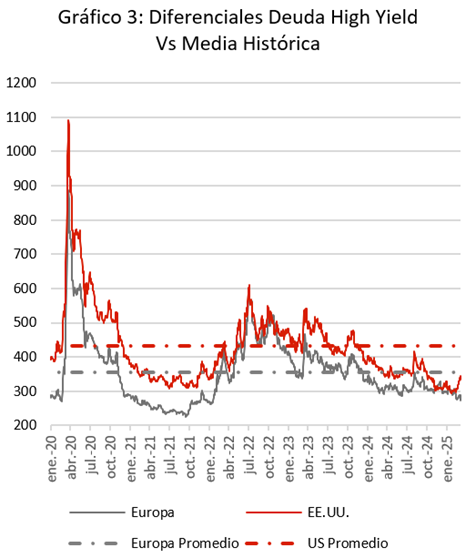

When this indicator drops below zero, riskier assets rarely generate positive returns, as the market's willingness to provide liquidity to companies (whether in the form of equity or debt) diminishes. While the current levels are nowhere near the negative levels seen in 2022, this is yet another sign that market confidence has suffered, and that the complacency established in lower credit quality corporate bonds (high yield) is beginning to feel the impact of uncertainty-driven volatility (chart 3).

Conclusion: There’s no reason to panic

Although developments in February and early March could change the outlook for the year, many of the factors at play are external to the market and difficult to predict or base investment decisions on. The four key pillars (growth, inflation, liquidity, and corporate earnings) point to a neutral market environment, despite slight deterioration in growth and liquidity in recent weeks.

On the bright side, there's the potential for a peace deal in Ukraine, Europe shaking off its stagnation—thanks in part to Trump's policies (even if his approach isn’t always politically correct)—and the US stepping back from tariff escalations to focus on the new president's pro-growth agenda.

One of the biggest changes in financial markets so far in 2025 is that diversification is paying off again. To some extent, we're better insulated from potential developments than in previous years, such as 2024, when only 15% of companies beat the S&P 500. This year, however, more than 60% of companies are outperforming the index.