The Fed and the ECB: on divergent paths

Redacción Mapfre

Eduardo García Castro, senior economist at MAPFRE Economics

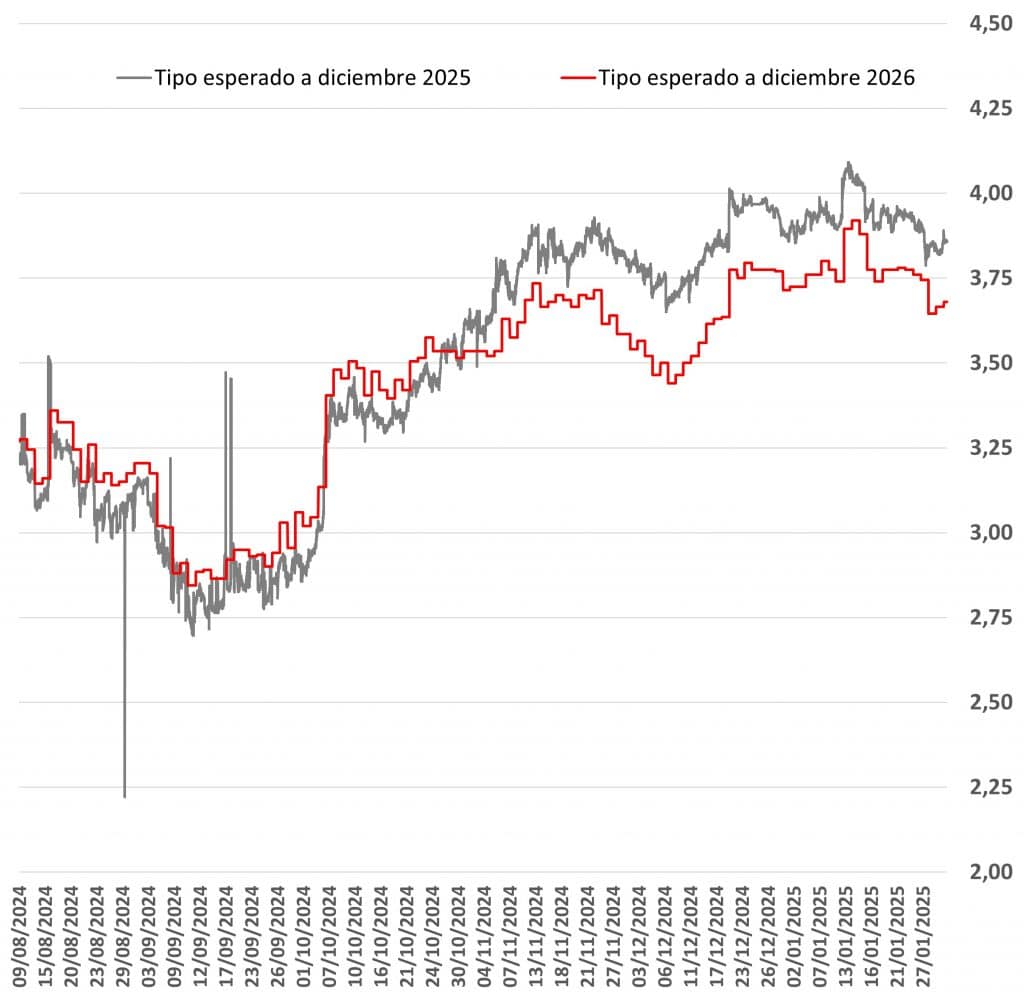

Investors have been very attentive this week to the Fed and ECB meetings. These are their main conclusions:

European Central Bank (ECB)

At its January meeting, the European Central Bank (ECB) announced a further 25 basis point (bps) cut in interest rates, placing the range at 3.15% for marginal lending, 2.90% for financing and 2.75% for deposit facilities. With regard to the balance sheet, it should be noted that no additional guidance was provided beyond that presented in December, when reinvestment under the PEPP were completely interrupted and the last TLTRO matured. This drainage has since left the role of the system's liquidity in the hands of the weekly credit facility (MRO) and, ultimately, the marginal facility (MLF), previously cut off as an access corridor. However, the still excessive reserves mean these tools are relegated to secondary status while weight is maintained on the interbank rate (€STR), a dynamic that has caused it to approximate the deposit rate (DFR), but which could soon change, either due to the continuation of balance sheet reductions or as a result of potential liquidity stress events.

Chart 1: Rate range forecasts

In the governing council’s statement, an extension of the December vision was presented, expressing concerns about economic stagnation and reaffirming its commitment to achieving the main objective, stability in prices, although it stressed that it is on the right track. Looking ahead, the narrative paves the way for continuing to make monetary policy more flexible in the future, but it exposes downside risks, both to discount a less promising path and to defend the need to maintain a certain level of caution. Support for the decision was unanimous, although as was seen in the subsequent press conference, the reality of the situation will become clearer in the near future on the back of new projections, indicating that the terminal rate has not yet been agreed on.

Assessment

Since the last forecast update and the subsequent rate cut, growth in the eurozone has remained slow, the erratic inflation path (again exposed to energy volatility), fiscal vulnerability has been latent (both due to the upcoming elections and the lack of budget approval) and the somewhat more complex geopolitical environment (tariffs and a new global trade environment are already part of the baseline scenario). Consequently, the ECB's stance may lose some consensus and encounter certain resistance among the members of the governing council as they approach the neutral range. In other words, although the road map remains on the table, there are less convincing signs that it can be kept intact in the future.

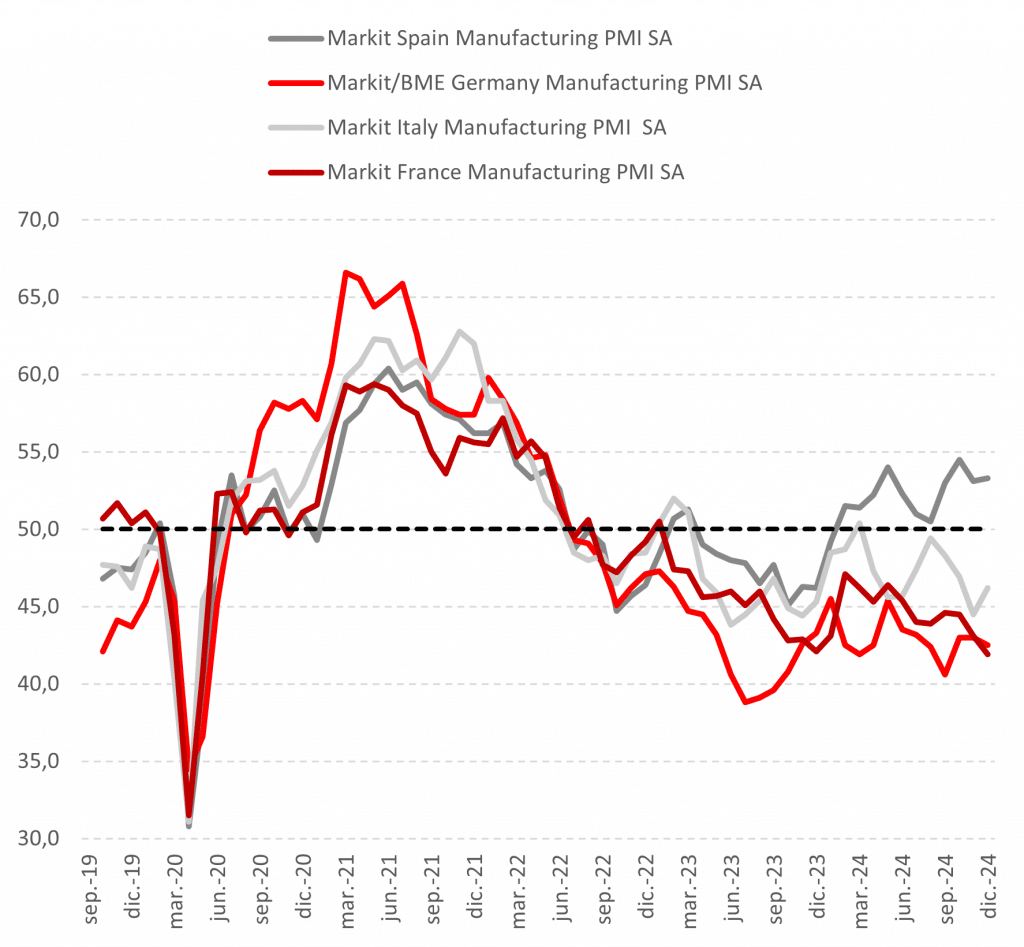

In terms of activity, the sustainability of recovery has remained fragile (advancing 0.0% in Q4) and shows that divergences are still a reality (the economies of Germany and France contracted -0.2% and -0.1%, respectively). As indicated by the latest PMI data, the manufacturing sector showed a slight improvement, but it continues to contract and be constrained by concerns about competitiveness. The services sector continues to expand and take the lead but continues to manifest a symptomatology of stabilization that shows that, by itself, it is unable to leave the stagnation behind (see Chart 2). The latest German IFO also pointed this out, with a more positive reading of the current situa-tion, but nonetheless accompanied by business climate expectations that continue to languish in their prospective vision.

Chart 2: PMIs Eurozone PMIs

Internally, consumption and investment engines are not firing on all pistons either, as shown by the high savings rates that have been reestablished against their peers. Although the falls in interest rates should begin to be partly evidenced (note the recent upturn in demand for credit), real salaries (linked to weak productivity) and expectations (linked to the adjoining of external and internal uncertainties) have not yet recovered the open gap in consumer confidence. This, contextualized from a full employment perspective like the current one, suggests that no significant rebound beyond the cyclical factor is on the cards.

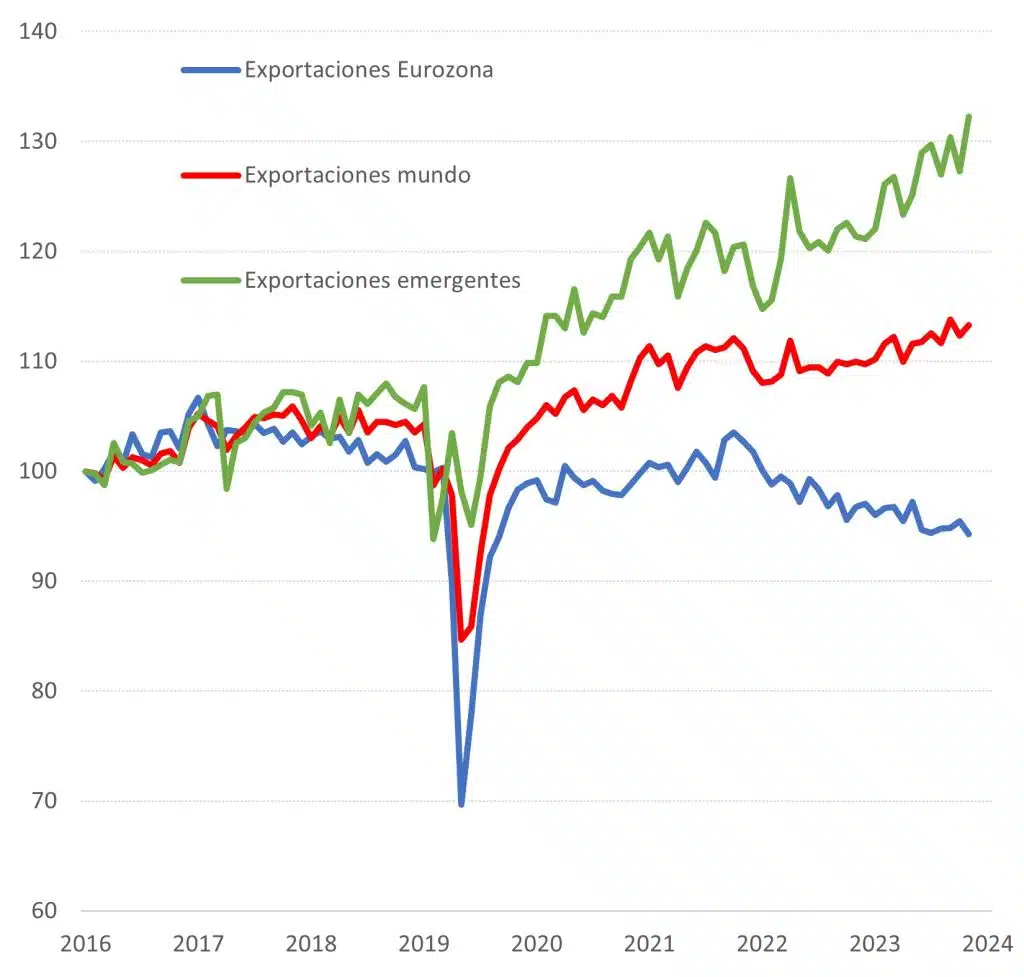

Externally, and despite a weaker euro, the rate of exports continues to lag behind the global pace, while supply chains continue to undergo transformation and roles of the different trading partners are redefined through near-shoring/friendshoring policies (see chart 3). This situation leads, to a certain extent, to a downward, selfperpetuating spiral. Each improvement in international competition exposes structural deficiencies and widens the competitive gap (widely mentioned by Draghi, Letta or the most recent Competitiveness Compass presented by the European Commission).

Gráfica 3: Exportaciones de Europa frente a otros

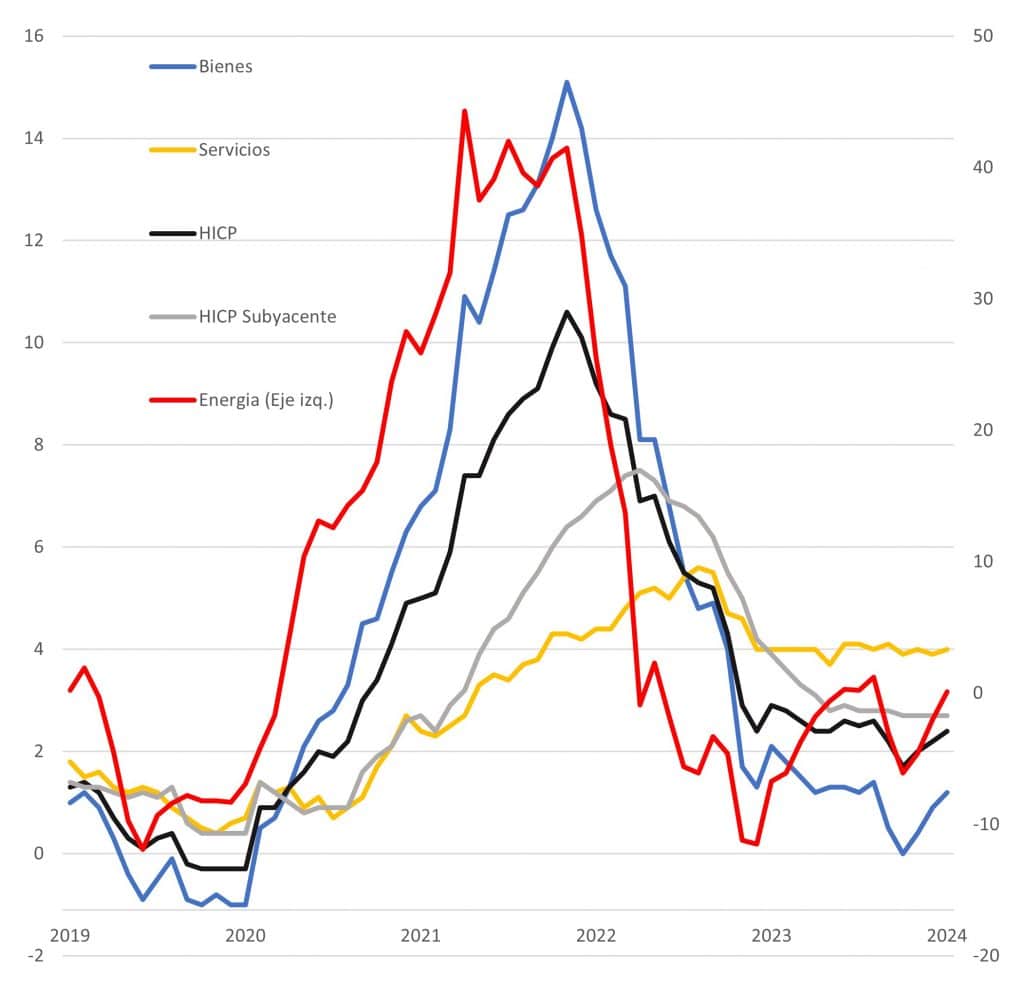

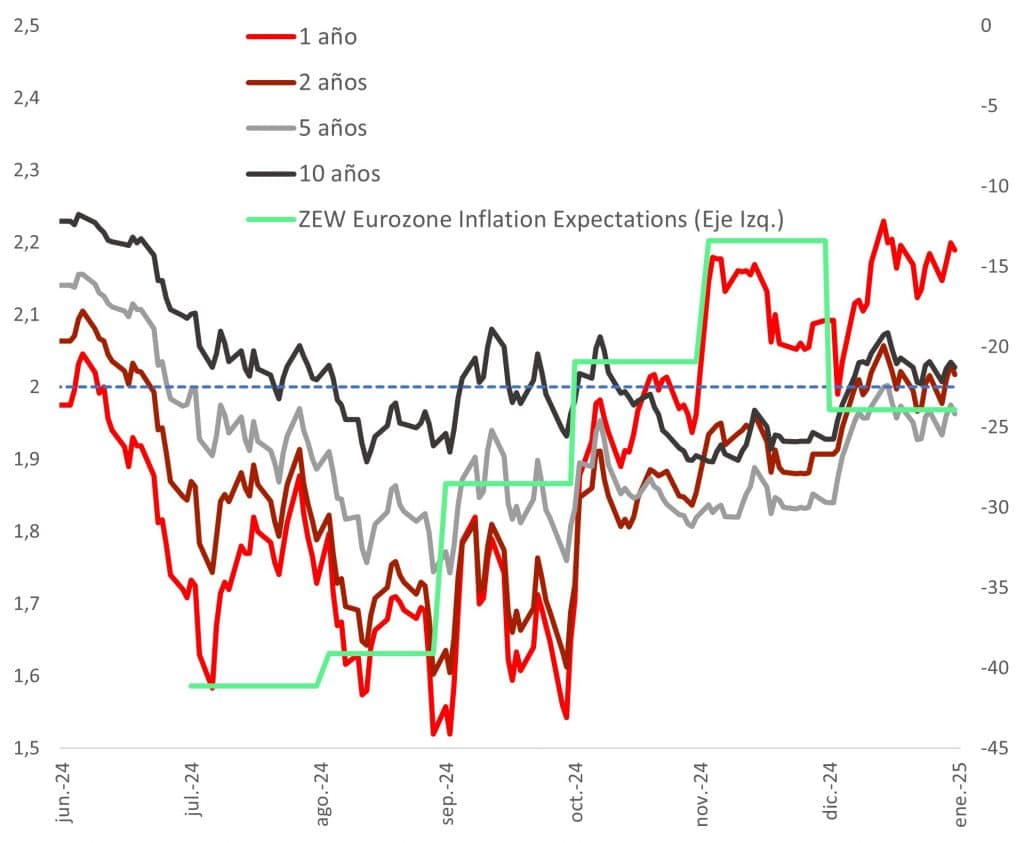

In terms of prices, general inflation rebounded in December to 2.4% YoY, while core inflation remained unchanged at 2.7% YoY. The rigidity of services was once again confirmed (4.0% YoY), energy became a positive contributor and food supplies, although with an intermonthly decrease, continued to progress at a rate of 2.9% YoY (see chart 4). This increase was broadly expected and remains consistent with the preliminary forecasts, so the capacity to surprise council members remains limited. On the other hand, and as shown by the increases in inflation expectations (see Chart 5), it is not yet appropriate to rule out the ECB's optionality wild card, at least until the picture regarding energy imports, salaries and tariff risks is clearer.

Chart 4: Inflation and its components

Chart 5: Inflation expectations (swaps y ZEW)

In terms of risks, and related to the foregoing, external fronts continue to hinder a com-plete change in the ECB's narrative. Whether due to energy price sensitivity or the possibility of appearing on the “tariff targets” list, the effects could be remarkable and could derail forecasts. In this regard, economic theory states that the exchange rate impact of tariffs should negatively affect the local currency against the dollar, which is known as competitive devaluation. With this gain, domestic production would be deviated to accommodate greater external demand while domestic prices would remain stable and import consumption would be deincentivized.

However, in an open economy like Europe with a structural energy and strategic raw materials deficit and a certain competitive lag, certain levels of foreign imports are still need-ed to supply these production increases. This could in turn mitigate the possibilities of ab-sorbing the impact provided by the devalua-tion mechanism itself if the weakening of the currency extends to its trading counterparts, such that the devalued currency results in imported inflation.

Conclusion

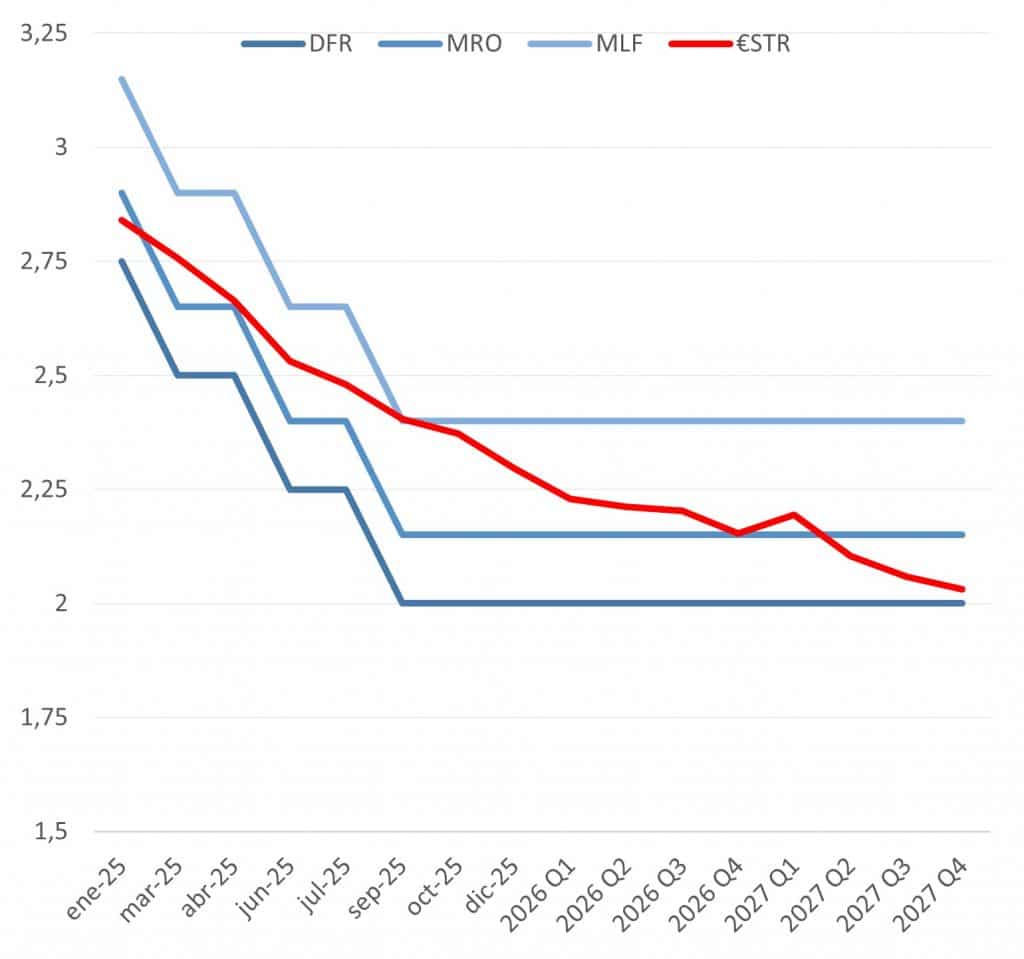

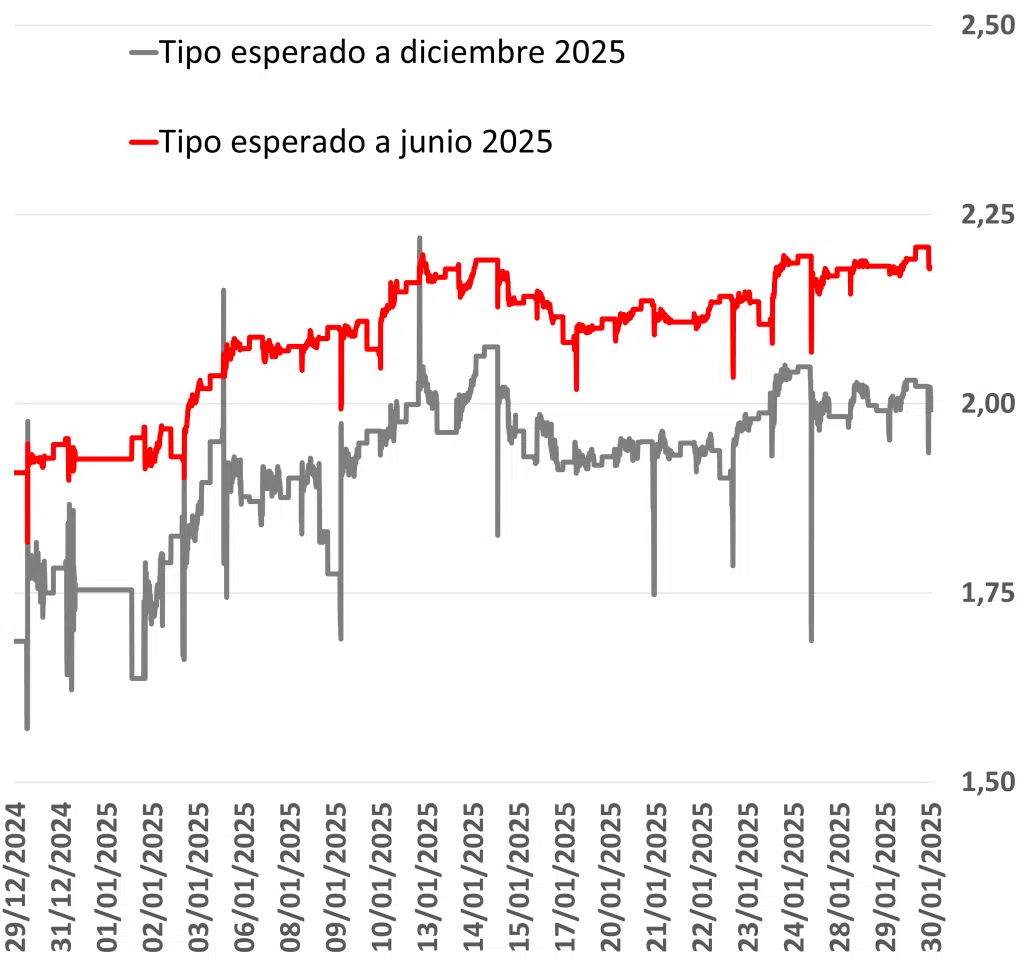

In conclusion, the macroeconomic outlook remains anemic, while the inflation target is somewhat closer, which makes it easier for the ECB to make good on its plans to cut rates. Therefore, the scenario of achieving monetary neutrality this same year remains quite plausi-ble (see Chart 6). However, uncertainty re-mains high, which is sufficiently urgent reason to maintain caution and, in parallel, to acceler-ate the internal discussion on the range within which the neutral interest rate rests.

Chart 6: Overnight indexed swaps

This approach requires an analysis that is not so dependent on current data and more founded on future assumptions, i.e., a modal rate or long term point of equilibrium that is high enough to ward off inflation but not so low that it stifles demand.

Thus, and given that the main objective of the ECB is stability of prices, it is predicted that caution will remain at the top of the agenda, at least until such time as it is confirmed that the appropriate range has been widely agreed on. As such, and with the aim of providing a constructive vision in this regard, MAPFRE Economics has just joined the ECB’s Survey of Monetary Analysts.

Within this discussion, there is a double divergence as a secular determinant for calcu-lating this terminal rate. On the one hand, potential growth seems to be on a lower growth path in response to the limited com-petitive capacity that lies in the industrial heartlands, which tilts the debate in favor of lower rates. This is also consistent with the interpretation of structurally weaker internal inflation, which also justifies lower rates. However, this relationship responds to global factors that increasingly underpin the argument for “competitive rates” or high rates. Therefore, as production faces existential challenges, imported inflation is linked to exogenous factors that exert pressure. As such, our secular horizon continues to visualize a landscape comprising limited potential growth, low inflation and less controllable external inflation, at least from a central bank perspective.

Federal Reserve

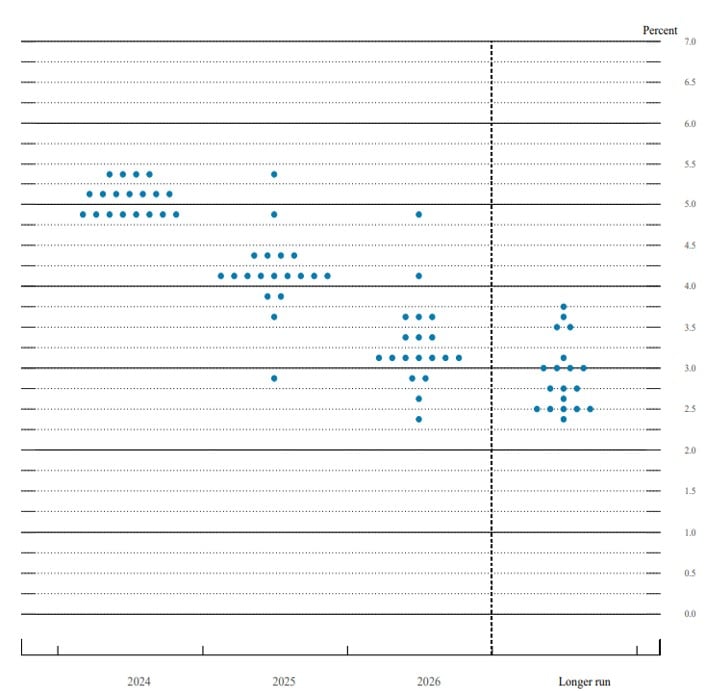

At its first meeting of the year, the United States Federal Reserve decided to keep official interest rates unchanged, holding the range at 4.25% - 4.50%, in line with what was expected by the market. Regarding the disclosure of expectations, a cautious forward-looking stance was maintained, closely resembling that presented last December, although with an additional wait-and-see bias to gain a clearer direction (see Chart 1). In more detail, two rate cuts of 25 basis points (bps) are projected for this year, with two additional cuts in 2026, aligning with a gradual pace of decline toward the long-term terminal rate, which remains around 3.0%.

Chart 1: Dot Plot

Regarding the quantitative adjustment of the balance sheet, it continues its course with no changes indicated, remaining at 2020 levels. Notably, to date, the Federal Reserve has reversed nearly half of the pandemic-era expansion, reducing its balance sheet by approximately $2.1 trillion, of which $1.5 trillion corresponds to Treasury bonds and $0.5 trillion to mortgage-backed securities (MBS). There was also no mention of the remaining liquidity lines opened to assist banks, which are nearing full depletion (see Chart 2).

Chart 2: Federal Reserve Balance Sheet

The communication stance remained firm, providing little additional information and emphasizing that, although inflation has declined, there is still room for improvement. Moreover, concerns about employment have proven to be more temporary than initially expected, aligning more closely with the strong momentum of the economy in terms of economic growth. Therefore, no immediate reaction is expected due to the lack of significant progress, nor is there a need to cut interest rates at this time.

Assessment

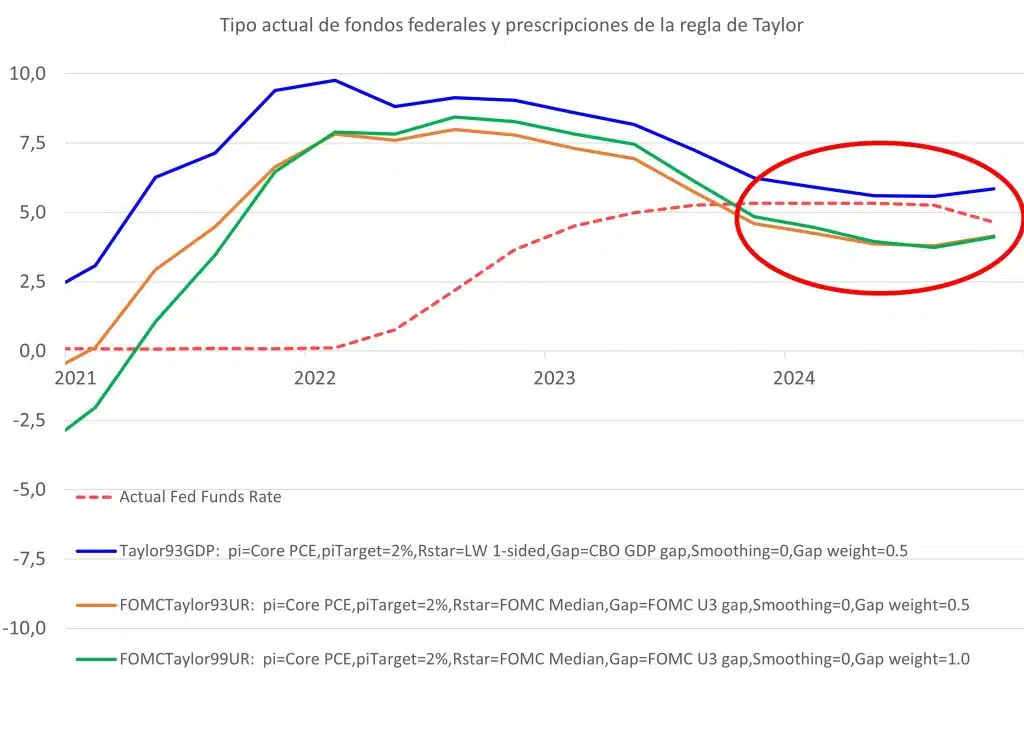

The main reading by the Federal Open Market Committee (FOMC) suggests that the December message is still in force and that it is therefore not necessary to resume interest rate cuts for the time being. The latest evidence on inflation remains somewhat concerning; however, employment-related concerns have eased, while growth metrics indicate that the economy continues to be resilient. Furthermore, when channeling these and other variables through the Taylor rule, they suggest that the current range of rates is appropriate and fully consistent with the current status of the economic cycle (see Chart 3).

Chart 3: Current and theoretical rate according to the Taylor rule

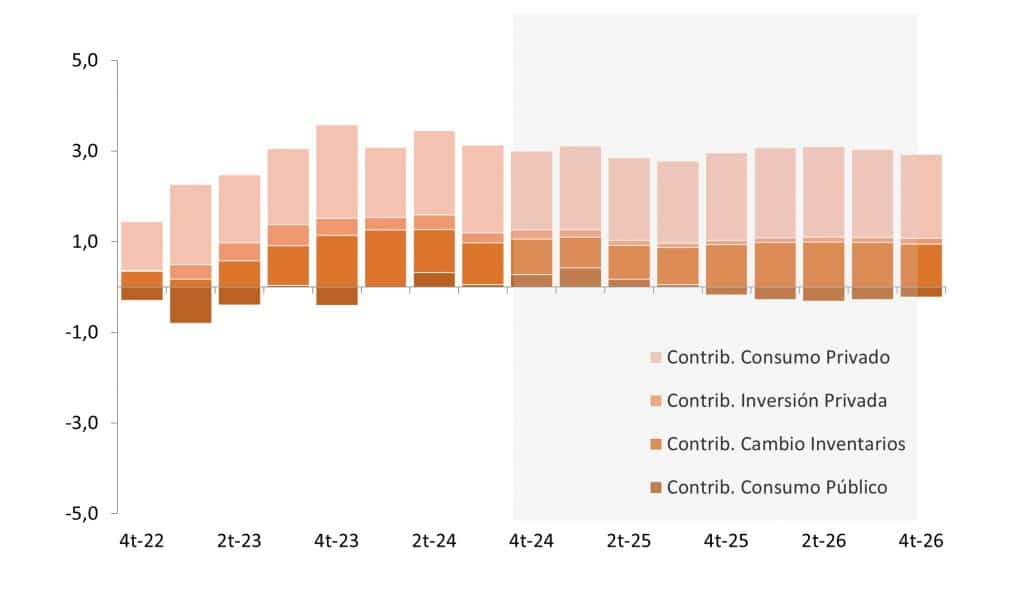

Analyzing the latest activity data, there remains a sense of optimism that the economy will continue expanding sustainably. The manufacturing PMI returned to expansionary territory, while the services PMI, though slowing, continued to show positive progress. Additionally, the ISM metric indicated consistent growth in employment and an improvement in production, which could suggest early signs of a positive trend shift in the industry. These figures contrast with the loss of momentum in the Leading Economic Index (LEI) for December, the decline in consumer confidence, and the slow-down in retail sales. Despite these mitigating factors, there is still no clear evidence to suggest that the U.S. “exceptionalism” will fade anytime soon (see Figure 4).

Chart 4: GDP growth estimates

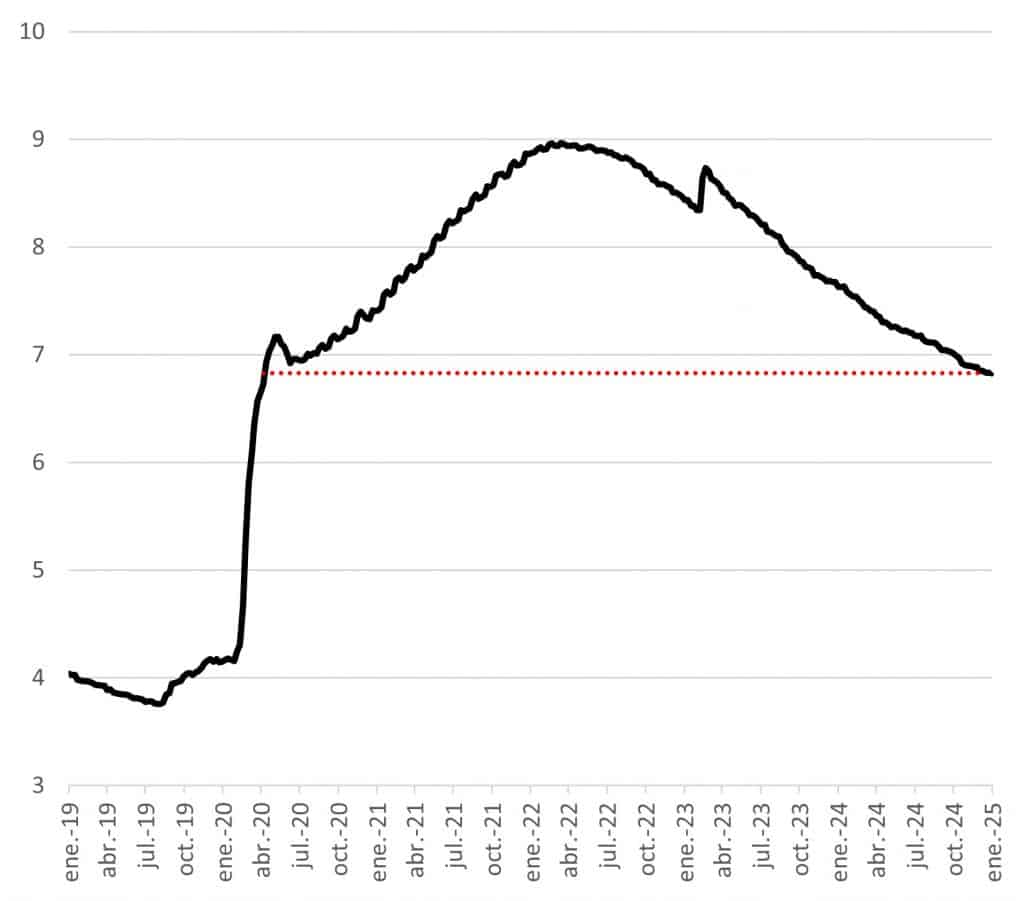

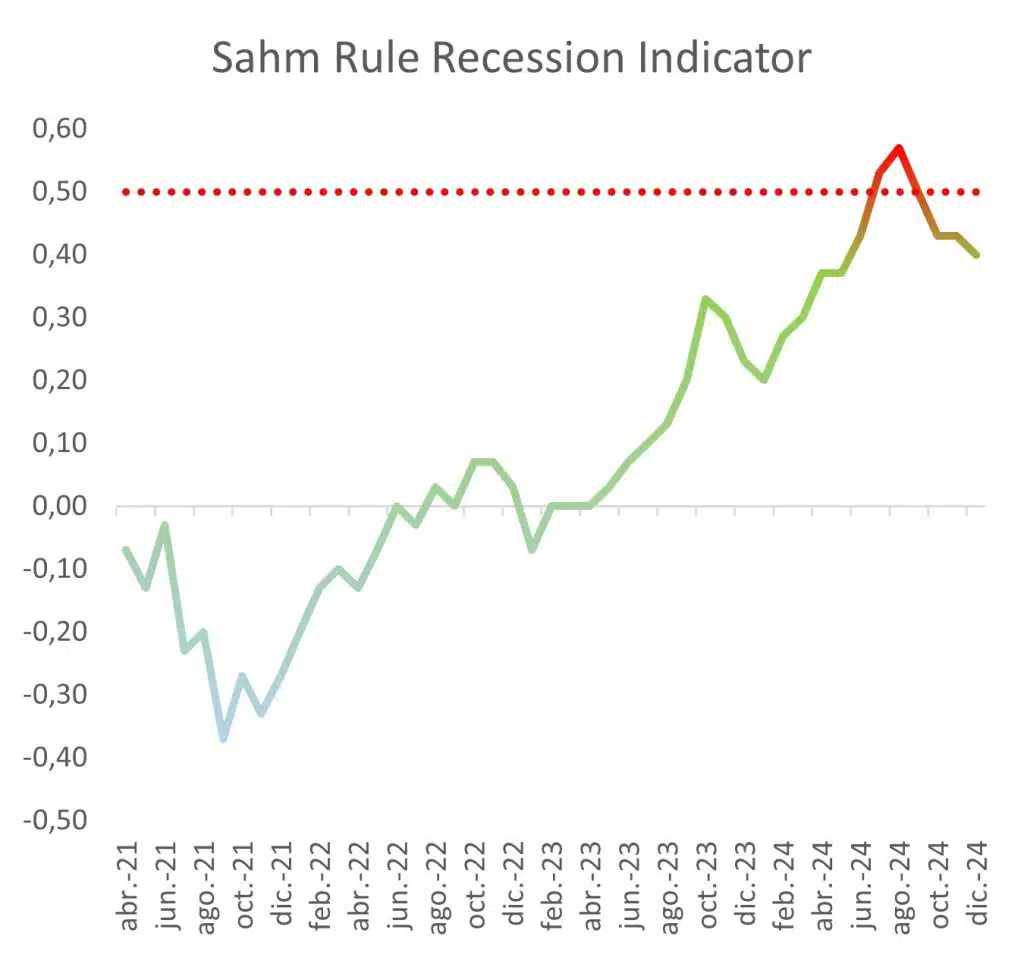

In terms of employment, the data remained strong: the unemployment rate fell to 4.1%, the Bureau of Labor Statistics (BLS) payroll report rose to 256,000, and job openings increased again in the JOLTS (Job Openings and Labor Turnover Survey) report. In other words, this alleviates concerns about the labor market and confirms that it remains consistent with a full employment dynamic. Weekly unemployment claims also do not present any new signals, showing only marginal increases so far this year, providing little indication of a shift in the labor market trend. As evidence of this, another recession indicator, the Sahm Rule, has returned to normal territory (see Figure 5).

Chart 5: Sahm Employment Rule and Deactivated Reces-sion Threshold

In terms of inflation, the last reading in December showed a new acceleration to 2.9% YoY and 3.2% YoY in the underlying inflation (which does not consider energy and food). Although the increase was widespread, notable sectors include housing (4.6% YoY), food (2.5% YoY), and monthly accelerations in both used cars (1.2% MoM) and energy (2.6% MoM). These categories remain negative on a year-over-year basis but suggest a degree of rigidity that persists in inflation and should be taken into account (see Figure 6).

Gráfica 6: Inflation by components

Additionally, in light of the electoral results from last November, a new factor arises to consider—the potential effects of the new domestic and foreign policy of the United States, which, at first glance, appears to align with a scenario of more growth and more inflation, but is undoubtedly uncertain. From a revisionist perspective, focusing on tariffs, the most immediate effect of these measures is their contribution to reducing the trade deficit, protecting domestic industry, boosting local employment, and countering international competition. These aspects help steer the economy toward a more favorable internal balance in the short term. However, the effects on potential output are much more complex to analyze, as they have somewhat counterproductive consequences, such as reduced exports, retaliatory measures from trading partners, fewer substitute goods available for consumers, and a shift of the initial imbalance abroad due to decreased international competitiveness.

On the other hand, in terms of prices, there is greater consensus on the future dynamics, with effects moving in the opposite direction. Higher prices are consistent in both the short and long term due to the reduced incentive for innovation, lack of competition, tariff barriers to entry, absence of substitute goods, and, to some extent, the establishment of consumers’ acceptance of local product prices.

In conclusion, the Federal Reserve usually establishes the most appropriate interest rate for each moment based on the analysis of the data present and the modeling of its behavior in the future, a dynamic that currently shows an appropriate balance with the decision not to introduce changes. However, this decision-making mechanism is fluid and subject to additional uncertainty, both in the short term, due to the immediate effects of these policies (migratory, regulatory, fiscal, and commercial) and in the long term, due to the incorporation of theoretical assumptions into the models that determine the terminal interest rate (see Chart 7).

Chart 7: Expected interest rates