"Monetary stimuli could cause the economic cycle to enter reflation mode"

Redacción Mapfre

Monthly report from MAPFRE Gestión Patrimonial

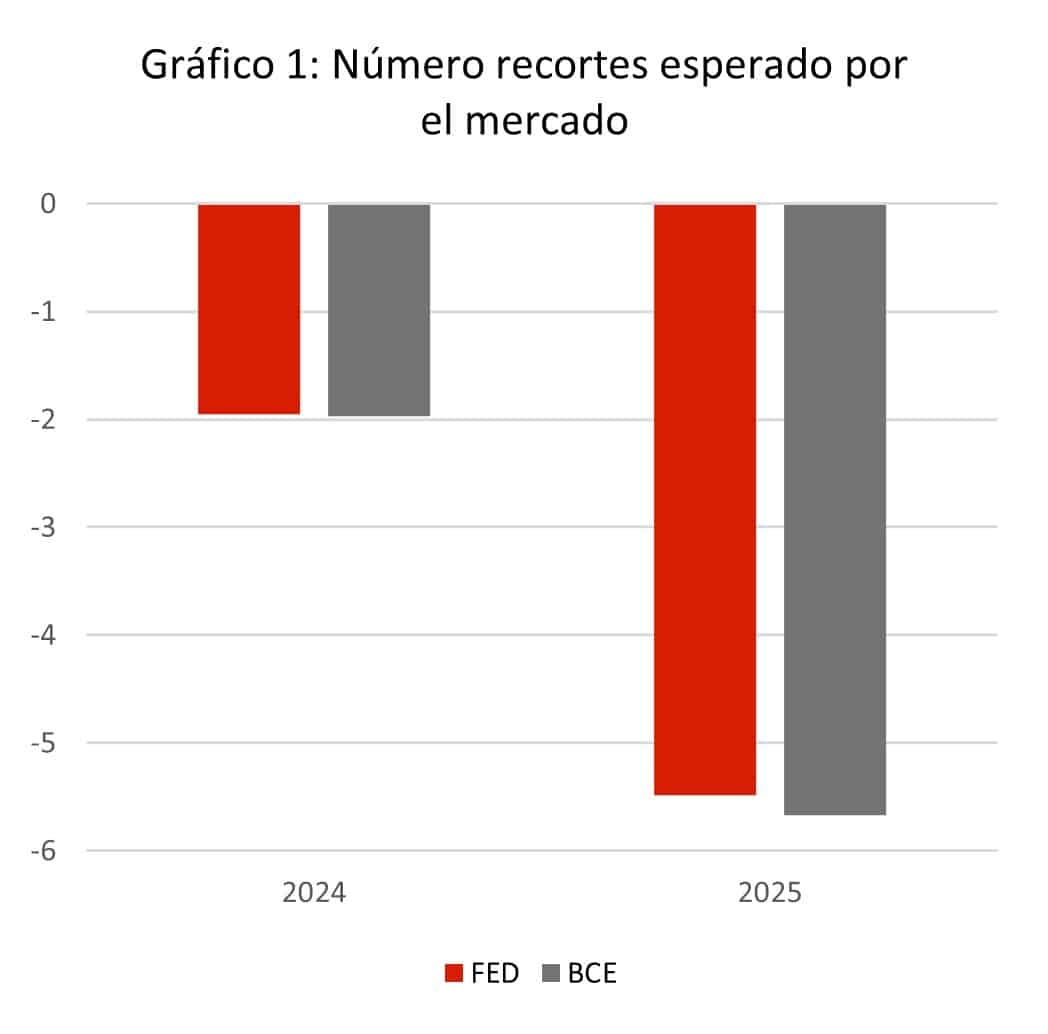

The expected and desired interest rate cut by the U.S. Federal Reserve (Fed) is now a reality. The primary U.S. monetary authority reduced rates by 50 basis points, catching much of the market off guard, as analysts had anticipated a cut of only 25 basis points. The European Central Bank (ECB) also reduced official interest rates as planned. We are in a market environment where the two most important central banks are starting to reduce official interest rates, which have remained at levels not seen for over two decades.

The market's reaction to these decisions has been positive for both bond prices—especially those in the shorter maturities—and equities, as these cuts are expected to lower the likelihood of a recession in the short to medium term. This is why we find ourselves in a favorable moment for the market, which could foster complacency—the primary risk we observe in the markets.

For months, we have been absorbing a very pessimistic narrative about the true state of various economies. However, they have managed to withstand high interest rates quite well. As in mountaineering, where most accidents happen on the descent, it would be wise to remain cautious even as interest rates begin their downward trend. We emphasize this because the market's interest rate cuts do not align with the current macroeconomic landscape.

In addition, the inflation that many consider 'dead' could resurface due to the very loose financial conditions, which will become even looser following the rate cuts by the FED, ECB, and now the People's Bank of China Monetary and fiscal stimuli from the two main economies (USA and China) would likely push the economic cycle into reflation, but from a much stronger starting point than in previous instances.

Macro reality is quite different

Fears raised by a series of weak macroeconomic data in the United States in August were quickly forgotten in September. The job market has once again surprised with the creation of over 250,000 new jobs last month, along with an upward revision of the previous month’s data. The unemployment rate dropped by one-tenth to 4.1%, while salaries increased above inflation. Thus, the labor market, which had become the focal point of concern for Fed Chairman Jerome Powell, provides relief and bolsters hopes of achieving the desired soft landing.

In fact, if we examine growth and inflation expectations, the market clearly reflects this scenario. In terms of growth, the forecast for 2025 in the United States remains flat at approximately 1.8%. While this may not be a particularly high figure, it can still be considered positive.

The greatest concerns are in Europe, particularly in its two largest economies: France and Germany. The former, due to political instability and a rapidly growing fiscal deficit, which even threatens its credit rating, while the latter is significantly impacted by rising energy costs and its dependence on China. Both would need a boost to align with the growth levels expected for the United States.

It is no surprise that the impact of the so-called 'Draghi Report' published on September 9, was significant. This report analyzed the current situation of the old continent and proposes specific measures to promote the European economy, focusing on innovation, decarbonization, and competitiveness to avoid falling behind the two major global powers: the United States and China. Beyond these problems in the functioning of the eurozone, the current macroeconomic outlook does not justify the scale and pace of interest rate cuts expected by the market.

Liquidity increases the speed of the decline

The laxity of the aforementioned financial conditions is closely linked to the ease of obtaining financing in the markets. In addition to the endogenous liquidity driven by the investment appetite of large financial institutions, there is the liquidity created in the system by central banks after a long period during which they withdrew money to curb inflation.

It is logical, therefore, to expect the opposite path in the coming months: if the Fed and ECB have begun to ease their monetary policies, it would be typical for them to support this easing with greater liquidity injections to facilitate the reduction of interest rates. This liquidity, in fact, is already reaching households and non-financial companies, as evidenced by the latest M2 money supply data in both the eurozone and the US. The main difference between the two regions is that, in the United States, this increase in liquidity is still being directed toward consumption and investment, while in Europe, the savings rate has risen. This may be due to a lack of short- and medium-term confidence in the European economy, as well as the attractive returns on monetary and short-term assets.

With lower interest rates in the medium term, it is highly likely that these savings will seek returns in other market assets or that confidence will return to European consumers, leading to increased consumption. This could lead us back to a risky scenario where inflation re-emerges as a problem, potentially halting interest rate cuts prematurely.

The “Whatever it takes” from China

September concluded with several stimuli announcements by Chinese authorities, triggering an extraordinary rally in stocks traded in both domestic markets and Hong Kong. In fact, at the end of the month, the Hang Seng stood as the stock index with the highest accumulated revaluation in 2024.

In true Mario Draghi style from his famous 2012 speech, where he stated he would take any measures necessary to 'save' the European economy, the Chinese government opted to launch a fiscal and monetary stimulus package to achieve its growth target of 5% while also restoring the confidence of Chinese households and businesses.

Among the most notable measures are a 50 basis point reduction in the reserve ratio that banks must maintain with the central bank, a 20 basis point reduction in the interest rate for bank financing, loans to companies for share buybacks, and direct cash transfers to low-income families to bolster spending. The combination of monetary aid with fiscal support would help achieve the three main objectives of the Chinese government: revitalizing the real estate market, increasing household wealth, and recapitalizing businesses, which in turn could restore the health of the banking sector.

These measures, though long anticipated, mark a new direction and a higher level of political support, as the Chinese government aims to revitalize the stock market. This strategy encourages households to channel their accumulated savings into investments, creating a wealth effect that also attracts foreign capital. Globally, these measures are reflationary and would increase the possibility of seeing an upturn in inflation next year.

Conclusion: Cautious optimism

Overall, the situation is positive, as the lowering of interest rates provides relief for growth that has been resilient in the face of a very restrictive monetary policy. Inflation continues to moderate, although it may not be as well-controlled as it seems. Energy prices, stimulus measures in China, and the return of liquidity could reignite inflation sooner rather than later, potentially undermining the significant number of rate cuts anticipated by the market. This is a risk to consider alongside geopolitical events and the upcoming earnings season, which begins in the coming weeks.