“The ECB returns from the summer break with news of additional interest rate cuts”

Redacción Mapfre

Eduardo García Castro, Senior Economist at MAPFRE Economics

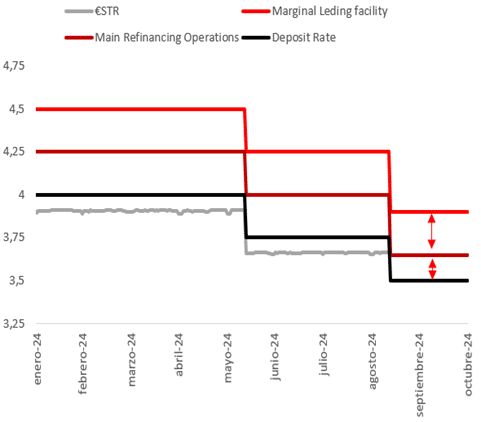

The European Central Bank (ECB) once again reduced interest rates by 25 basis points (bps) at its September meeting. In addition, and as part of the strategic review previously announced, the margin between the different rates has been reduced, with the lending rate standing at 3.90%, the principal rate at 3.65% and the deposit facility rate at 3.50%.

This change in the interest rate spread, which will come into force on September 18, although representing a technical measure for adjusting the spread between the rate at which banks can access one- and seven-day lending, is immaterial, given the effect of excess liquidity on the €STR, a representative Eurozone index that reflects the cost of financing for Eurozone banks on the wholesale markets of the main lending institutions in one-day unsecured operations (deposits).

However, in the future, the measure will help to monitor the health of the interbank rate, with an approach that places an emphasis on the future behavior of the spreads as this excess liquidity continues to drain.

Official interest rate spread

Source: MAPFRE Economics, based on ECB data

There have been no developments on the balance sheet side, so the existing roadmap to continue reducing its size at a measured and predictable pace under the Asset Purchase Program (APP), as well as under the Pandemic Emergency Purchase Program (PEPP) remains in place, giving way to a break in reinvestments at the end of the year (the entire principal is no longer reinvested) and a 7.5 billion euro reduction process starting in the second half of the year.

At a macroeconomic level, a new series of forecasts have been released that are essentially the same as those published in June. In fact, the average inflation forecast remains unchanged, at 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, while as for core inflation, this forecast has been increased by one tenth in the first two years, to 2.9% this year, 2.3% in 2025 and 2.0% in 2026.

Concerning growth, the forecast is slightly down and has been reduced by one tenth to 0.8% in 2024, another tenth to 1.3% in 2025 and an additional tenth in 2026 to 1.5%. Regarding future guidance, a cautious stance remains; this will depend on data and remains far from offering a clear commitment, while retaining some ambiguity and the option of intervening more forcefully should downside risks materialize.

On the positive side, inflation looks set to continue to support the argument that price pressures have been brought under control. Specifically, headline inflation fell to 2.2% in August (from 2.6% in July), on account of lower prices in terms of energy, food and durable goods, alleviating concerns about service inflation that remains somewhat unpredictable.

Another positive can be taken from the salary indicator, although this should be left in quarantine, despite the significant drop in data for the second quarter (3.6%). This can be attributed to the importance of single payments in some countries and the staggered nature of salary adjustments. In fact, the results of collective bargaining in several important sectors (notably including the German industrial sector) have yet to be reflected, which could reduce optimism regarding the pace of wage deceleration in the second half of the year.

Fiscal policy remains slightly out of sync with the sustainability thesis proposed by institutions including but not limited to the European Commission; this leaves the door ajar to additional steps towards restriction in the future and structural reforms until a certain balance and competitiveness is restored, even should this require the need for excessive deficit measures to be taken. If this conundrum is resolved, the approach by the ECB in the future is much more predictable, as it avoids focusing attention on interest rate spreads and moves away from the TPI (Transmission Protection Instrument) trigger.

In a macroeconomic setting, the economy seems to remain buoyant and on the path set towards a cyclical, rather than structural, recovery, although without the necessary momentum for this having been achieved as yet. Growth data for the second quarter, still revised downwards, has cleared up fears about the worst-case scenario, while high-frequency and prospective indicators concur that the general trend will continue within a context of continuity and sluggishness in the coming months.

Regarding secular trends, the most recent person to reflect on the “slow agony” ahead for the European Union was the former president of the ECB, Mario Draghi, in his latest report. It contains a wide range of ambitious proposals that combine the issuance of more common funds, with which to face the challenges ahead, combined with greater speed and political cohesion as a recipe against stagnation.

These measures for coordinating a new expansion of public spending with a view to enhancing efficiency, despite having the potential to combat secular stagnation by stimulating demand, from a broader perspective, may not be as effective against current stagflation, i.e. stimulating and resolving inefficiencies on the supply side. To achieve competitiveness, a private initiative to satisfy real needs and return the market to a state of equilibrium may be needed.

In short, the ECB has returned from the summer break with news of additional interest rate cuts, as well as announcing space to refine technical aspects of monetary policy tools. Inflation is more benign; salaries are less of a concern and growth is acceptable to a certain extent.

Looking to the future, evidence will be needed to make new cuts official, which is why questions remain as regards the chain of swaps. A more cautious approach would advocate for continuing to slow down the process and waiting until December for further rate cuts, while leaving the door open to acting in October if necessary. Such expectations would work in favor of the euro, keeping rate spreads contained in comparison to the dollar, even more so when considering that data from the United States is more “reassuring”, compared to the sluggishness in the fundamentals of a structurally slow Eurozone showing signs of risk chronicification.